Key Insights

The European LiDAR market is experiencing robust growth, driven by increasing adoption across various sectors. The market, valued at approximately €X million in 2025 (assuming a logical extrapolation from the provided CAGR of 23.60% and a known 2019-2024 period), is projected to reach €Y million by 2033, exhibiting a compound annual growth rate exceeding 20%. This expansion is fueled primarily by the automotive industry's growing reliance on autonomous driving technologies, necessitating advanced sensing solutions like LiDAR for object detection and navigation. Furthermore, the engineering and surveying sectors are leveraging LiDAR for precise 3D mapping and infrastructure monitoring, boosting market demand. Government initiatives promoting smart cities and infrastructure development across Europe further contribute to the market's upward trajectory.

Despite the optimistic outlook, several challenges exist. The high initial investment cost of LiDAR systems, along with the need for specialized expertise to operate and interpret the data, can act as restraints. Competition among established players and new entrants in the market is also intense, leading to price pressure. However, ongoing technological advancements, such as the development of more compact, cost-effective LiDAR sensors, are expected to mitigate these challenges and accelerate market penetration in the coming years. The segment breakdown shows strong growth across aerial and ground-based LiDAR systems, with increasing demand for advanced components like GPS and high-resolution laser scanners. Germany, the United Kingdom, and France are key markets within Europe, contributing significantly to the overall regional growth.

Europe LiDAR Industry Market Report: 2019-2033

This comprehensive report provides an in-depth analysis of the European LiDAR industry, offering invaluable insights for stakeholders seeking to navigate this rapidly evolving market. Covering the period from 2019 to 2033, with a focus on 2025, this report dissects market trends, technological advancements, and competitive dynamics to provide a clear picture of current and future opportunities. The study includes detailed segmentation by product (Aerial LiDAR, Ground-based LiDAR), component (GPS, Laser Scanners, Inertial Measurement Unit, Other Components), end-user industry (Engineering, Automotive, Industrial, Aerospace and Defense), and country (United Kingdom, Germany, Spain, Netherlands, France, Belgium, Rest of Europe). Expect robust data-driven analysis, including market size projections reaching xx Million by 2033.

Europe LiDAR Industry Market Composition & Trends

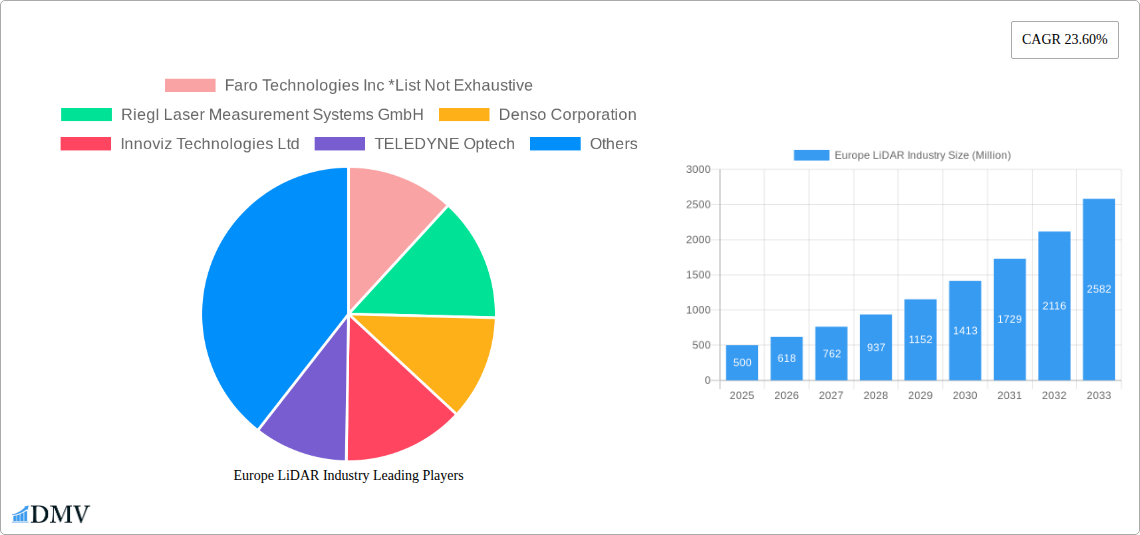

The European LiDAR market is characterized by a moderately concentrated landscape, with key players like Faro Technologies Inc, Riegl Laser Measurement Systems GmbH, and Velodyne Lidar Inc. holding significant market share. However, the emergence of innovative startups and the increasing adoption of LiDAR technology across various sectors are fostering a dynamic competitive environment. The market share distribution is expected to evolve significantly over the forecast period due to several factors.

- Market Concentration: The top 5 players hold approximately xx% of the market share in 2025, with a projected decline to xx% by 2033 due to increased competition.

- Innovation Catalysts: Ongoing R&D in MEMS technology, AI-driven data processing, and solid-state LiDAR are driving market innovation.

- Regulatory Landscape: The European Union's focus on autonomous driving and digitalization is creating favorable regulatory conditions, boosting LiDAR adoption.

- Substitute Products: While radar and camera systems compete, LiDAR's superior 3D mapping capabilities provide a distinct advantage, limiting substitution.

- End-User Profiles: Automotive, engineering, and mapping industries are key end-users, driving substantial demand for high-performance LiDAR systems.

- M&A Activities: The total value of M&A deals in the European LiDAR market between 2019 and 2024 reached approximately xx Million, indicating consolidation trends within the industry.

Europe LiDAR Industry Industry Evolution

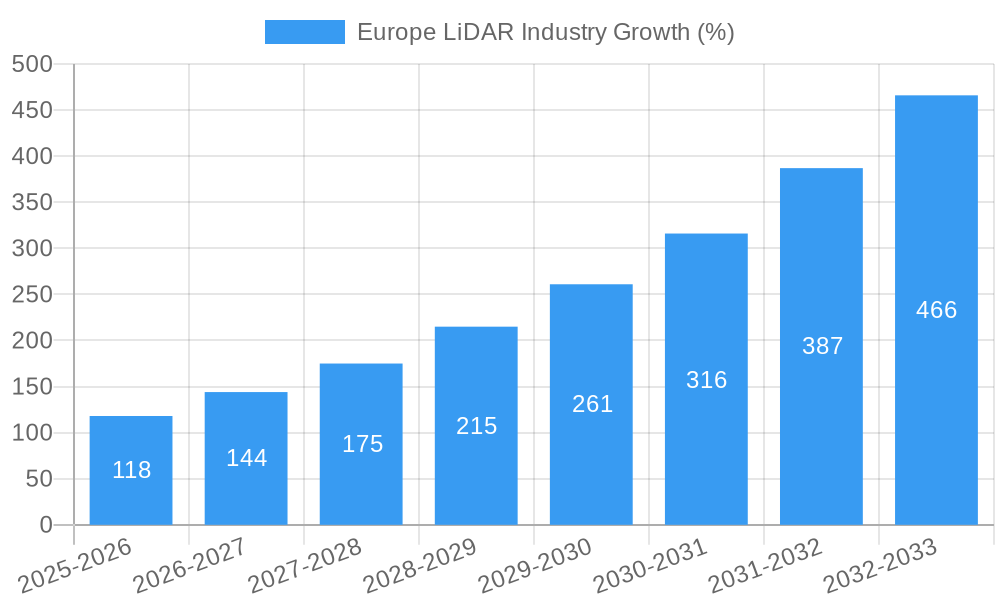

The European LiDAR market has witnessed exponential growth over the historical period (2019-2024), with a Compound Annual Growth Rate (CAGR) of xx%. This growth trajectory is expected to continue throughout the forecast period (2025-2033), driven by several key factors. The automotive sector's rapid embrace of Advanced Driver-Assistance Systems (ADAS) and autonomous driving technologies is a primary driver. Technological advancements, particularly in solid-state LiDAR and improved processing capabilities, are reducing costs and enhancing performance, thereby expanding the market's addressable applications. The increasing demand for precise mapping and surveying across various sectors is further propelling growth. This includes infrastructure development, environmental monitoring, and precision agriculture. The adoption rate of LiDAR technology in the automotive sector is projected to increase from xx% in 2024 to xx% in 2033. The market's evolution is also influenced by shifting consumer demands for safer and more efficient transportation solutions, which heavily rely on LiDAR technology for enhanced perception and navigation capabilities. The total market size is expected to reach xx Million by 2033.

Leading Regions, Countries, or Segments in Europe LiDAR Industry

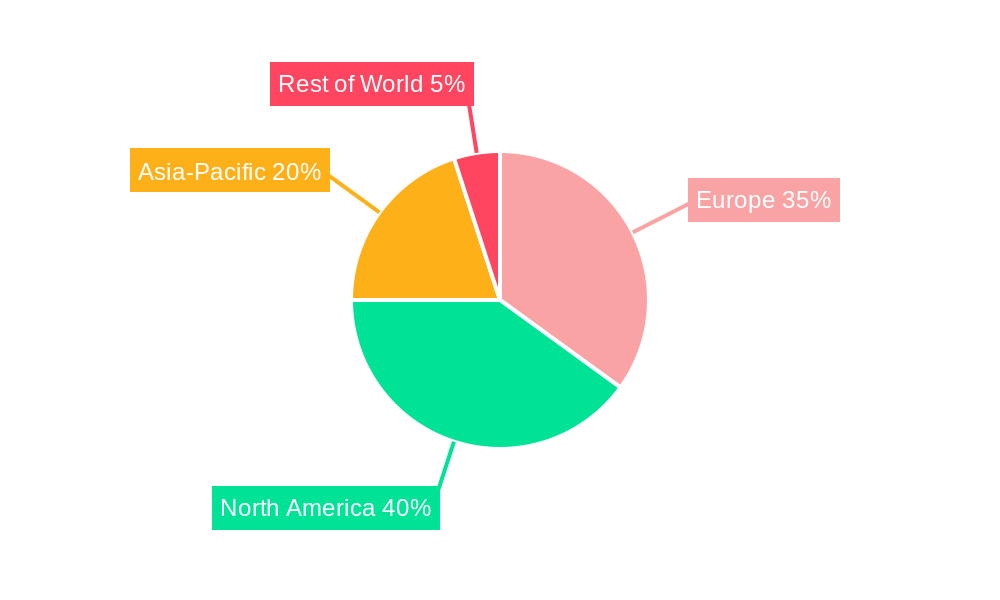

The automotive sector is currently the dominant end-user industry for LiDAR in Europe, accounting for xx% of the total market revenue in 2025. Germany and the United Kingdom are leading countries due to their robust automotive industries and supportive regulatory environments. Within the product segment, Ground-based LiDAR holds a larger market share than Aerial LiDAR due to widespread use in surveying, mapping, and construction.

- Key Drivers for Automotive Sector Dominance:

- High investment in autonomous vehicle development.

- Stringent safety regulations promoting ADAS adoption.

- Growing demand for high-precision object detection.

- Key Drivers for Germany and UK Dominance:

- Established automotive manufacturing hubs.

- Government support for technological advancements in autonomous driving.

- Presence of major LiDAR manufacturers and R&D facilities.

- Ground-based LiDAR Market Leadership:

- Widespread application in surveying and mapping.

- Relatively lower cost compared to aerial LiDAR.

- Easier deployment and accessibility.

Europe LiDAR Industry Product Innovations

Recent innovations include the development of smaller, lighter, and more cost-effective solid-state LiDAR systems, eliminating the need for complex mechanical parts. This enhances reliability and reduces manufacturing costs. The integration of AI and machine learning algorithms is improving data processing speed and accuracy, enabling real-time object recognition and classification. These advancements are expanding LiDAR's applications into areas previously inaccessible, such as robotics, smart cities, and industrial automation. The unique selling proposition of these new systems lies in their improved accuracy, longer ranges, and reduced power consumption, leading to a higher return on investment.

Propelling Factors for Europe LiDAR Industry Growth

Technological advancements, such as the development of solid-state LiDAR and improved sensor fusion techniques, are key growth drivers. Government initiatives supporting autonomous driving and smart city development are creating favorable market conditions. The increasing demand for precise mapping and 3D modeling in infrastructure projects and environmental monitoring also fuels market growth. Economic factors, such as increased investment in research and development, contribute to market expansion.

Obstacles in the Europe LiDAR Industry Market

High initial costs of LiDAR systems remain a significant barrier, particularly for small and medium-sized enterprises. Supply chain disruptions, caused by geopolitical instability and component shortages, can impact production and delivery timelines. Intense competition among established players and emerging startups creates pricing pressures, impacting profit margins. Regulatory uncertainties concerning data privacy and safety standards also pose challenges.

Future Opportunities in Europe LiDAR Industry

The integration of LiDAR with other sensor technologies, such as radar and cameras, is expected to create new opportunities. The expanding adoption of LiDAR in robotics and industrial automation presents significant growth potential. New markets, such as precision agriculture and environmental monitoring, are emerging as promising areas for LiDAR deployment. Developments in edge computing and AI will improve real-time data processing capabilities and expand the application range of LiDAR technologies.

Major Players in the Europe LiDAR Industry Ecosystem

- Faro Technologies Inc

- Riegl Laser Measurement Systems GmbH

- Denso Corporation

- Innoviz Technologies Ltd

- TELEDYNE Optech

- Quanergy Systems Inc

- Phantom Intelligence Inc

- Velodyne Lidar Inc

- Geoslam

- Trimble Inc

- Topcon Corporation

- Sick Ag

- Neptec Technologies Corp

- Leica Geosystems Ag

Key Developments in Europe LiDAR Industry Industry

- June 2022: Stellantis selects Valeo's third-generation LiDAR for Level 3 autonomous vehicles, signifying a major step towards widespread adoption of LiDAR in the automotive industry.

- January 2022: Blickfeld launches Qb2, a smart LiDAR integrating software and hardware, streamlining data capture and processing. This innovation simplifies LiDAR deployment and reduces operational costs.

Strategic Europe LiDAR Industry Market Forecast

The European LiDAR market is poised for sustained growth, driven by technological advancements, supportive regulatory frameworks, and increasing demand across various sectors. The market's expansion into new applications, such as robotics and smart infrastructure, will further fuel growth. Continued innovation in solid-state LiDAR and sensor fusion will enhance performance and reduce costs, making LiDAR technology more accessible and affordable. The market's projected size of xx Million by 2033 reflects this positive outlook and signifies substantial opportunities for market participants.

Europe LiDAR Industry Segmentation

-

1. Product

- 1.1. Aerial LiDAR

- 1.2. Ground-based LiDAR

-

2. Component

- 2.1. GPS

- 2.2. Laser Scanners

- 2.3. Inertial Measurement Unit

- 2.4. Other Components

-

3. End-user Industry

- 3.1. Engineering

- 3.2. Automotive

- 3.3. Industrial

- 3.4. Aerospace and Defense

Europe LiDAR Industry Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

Europe LiDAR Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 23.60% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Fast Paced Developments and Increasing Applications of Drones; Increasing Adoption in the Automotive Industry

- 3.3. Market Restrains

- 3.3.1. High Cost of the LiDAR Systems

- 3.4. Market Trends

- 3.4.1. Engineering Industry to Hold Considerable Market Share

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Europe LiDAR Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Product

- 5.1.1. Aerial LiDAR

- 5.1.2. Ground-based LiDAR

- 5.2. Market Analysis, Insights and Forecast - by Component

- 5.2.1. GPS

- 5.2.2. Laser Scanners

- 5.2.3. Inertial Measurement Unit

- 5.2.4. Other Components

- 5.3. Market Analysis, Insights and Forecast - by End-user Industry

- 5.3.1. Engineering

- 5.3.2. Automotive

- 5.3.3. Industrial

- 5.3.4. Aerospace and Defense

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by Product

- 6. Germany Europe LiDAR Industry Analysis, Insights and Forecast, 2019-2031

- 7. France Europe LiDAR Industry Analysis, Insights and Forecast, 2019-2031

- 8. Italy Europe LiDAR Industry Analysis, Insights and Forecast, 2019-2031

- 9. United Kingdom Europe LiDAR Industry Analysis, Insights and Forecast, 2019-2031

- 10. Netherlands Europe LiDAR Industry Analysis, Insights and Forecast, 2019-2031

- 11. Sweden Europe LiDAR Industry Analysis, Insights and Forecast, 2019-2031

- 12. Rest of Europe Europe LiDAR Industry Analysis, Insights and Forecast, 2019-2031

- 13. Competitive Analysis

- 13.1. Market Share Analysis 2024

- 13.2. Company Profiles

- 13.2.1 Faro Technologies Inc *List Not Exhaustive

- 13.2.1.1. Overview

- 13.2.1.2. Products

- 13.2.1.3. SWOT Analysis

- 13.2.1.4. Recent Developments

- 13.2.1.5. Financials (Based on Availability)

- 13.2.2 Riegl Laser Measurement Systems GmbH

- 13.2.2.1. Overview

- 13.2.2.2. Products

- 13.2.2.3. SWOT Analysis

- 13.2.2.4. Recent Developments

- 13.2.2.5. Financials (Based on Availability)

- 13.2.3 Denso Corporation

- 13.2.3.1. Overview

- 13.2.3.2. Products

- 13.2.3.3. SWOT Analysis

- 13.2.3.4. Recent Developments

- 13.2.3.5. Financials (Based on Availability)

- 13.2.4 Innoviz Technologies Ltd

- 13.2.4.1. Overview

- 13.2.4.2. Products

- 13.2.4.3. SWOT Analysis

- 13.2.4.4. Recent Developments

- 13.2.4.5. Financials (Based on Availability)

- 13.2.5 TELEDYNE Optech

- 13.2.5.1. Overview

- 13.2.5.2. Products

- 13.2.5.3. SWOT Analysis

- 13.2.5.4. Recent Developments

- 13.2.5.5. Financials (Based on Availability)

- 13.2.6 Quanergy Systems Inc

- 13.2.6.1. Overview

- 13.2.6.2. Products

- 13.2.6.3. SWOT Analysis

- 13.2.6.4. Recent Developments

- 13.2.6.5. Financials (Based on Availability)

- 13.2.7 Phantom Intelligence Inc

- 13.2.7.1. Overview

- 13.2.7.2. Products

- 13.2.7.3. SWOT Analysis

- 13.2.7.4. Recent Developments

- 13.2.7.5. Financials (Based on Availability)

- 13.2.8 Velodyne Lidar Inc

- 13.2.8.1. Overview

- 13.2.8.2. Products

- 13.2.8.3. SWOT Analysis

- 13.2.8.4. Recent Developments

- 13.2.8.5. Financials (Based on Availability)

- 13.2.9 Geoslam

- 13.2.9.1. Overview

- 13.2.9.2. Products

- 13.2.9.3. SWOT Analysis

- 13.2.9.4. Recent Developments

- 13.2.9.5. Financials (Based on Availability)

- 13.2.10 Trimble Inc

- 13.2.10.1. Overview

- 13.2.10.2. Products

- 13.2.10.3. SWOT Analysis

- 13.2.10.4. Recent Developments

- 13.2.10.5. Financials (Based on Availability)

- 13.2.11 Topcon Corporation

- 13.2.11.1. Overview

- 13.2.11.2. Products

- 13.2.11.3. SWOT Analysis

- 13.2.11.4. Recent Developments

- 13.2.11.5. Financials (Based on Availability)

- 13.2.12 Sick Ag

- 13.2.12.1. Overview

- 13.2.12.2. Products

- 13.2.12.3. SWOT Analysis

- 13.2.12.4. Recent Developments

- 13.2.12.5. Financials (Based on Availability)

- 13.2.13 Neptec Technologies Corp

- 13.2.13.1. Overview

- 13.2.13.2. Products

- 13.2.13.3. SWOT Analysis

- 13.2.13.4. Recent Developments

- 13.2.13.5. Financials (Based on Availability)

- 13.2.14 Leica Geosystems Ag

- 13.2.14.1. Overview

- 13.2.14.2. Products

- 13.2.14.3. SWOT Analysis

- 13.2.14.4. Recent Developments

- 13.2.14.5. Financials (Based on Availability)

- 13.2.1 Faro Technologies Inc *List Not Exhaustive

List of Figures

- Figure 1: Europe LiDAR Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Europe LiDAR Industry Share (%) by Company 2024

List of Tables

- Table 1: Europe LiDAR Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Europe LiDAR Industry Revenue Million Forecast, by Product 2019 & 2032

- Table 3: Europe LiDAR Industry Revenue Million Forecast, by Component 2019 & 2032

- Table 4: Europe LiDAR Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 5: Europe LiDAR Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 6: Europe LiDAR Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 7: Germany Europe LiDAR Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: France Europe LiDAR Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Italy Europe LiDAR Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: United Kingdom Europe LiDAR Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: Netherlands Europe LiDAR Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: Sweden Europe LiDAR Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: Rest of Europe Europe LiDAR Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Europe LiDAR Industry Revenue Million Forecast, by Product 2019 & 2032

- Table 15: Europe LiDAR Industry Revenue Million Forecast, by Component 2019 & 2032

- Table 16: Europe LiDAR Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 17: Europe LiDAR Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 18: United Kingdom Europe LiDAR Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 19: Germany Europe LiDAR Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: France Europe LiDAR Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 21: Italy Europe LiDAR Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 22: Spain Europe LiDAR Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 23: Netherlands Europe LiDAR Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 24: Belgium Europe LiDAR Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 25: Sweden Europe LiDAR Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 26: Norway Europe LiDAR Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 27: Poland Europe LiDAR Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 28: Denmark Europe LiDAR Industry Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe LiDAR Industry?

The projected CAGR is approximately 23.60%.

2. Which companies are prominent players in the Europe LiDAR Industry?

Key companies in the market include Faro Technologies Inc *List Not Exhaustive, Riegl Laser Measurement Systems GmbH, Denso Corporation, Innoviz Technologies Ltd, TELEDYNE Optech, Quanergy Systems Inc, Phantom Intelligence Inc, Velodyne Lidar Inc, Geoslam, Trimble Inc, Topcon Corporation, Sick Ag, Neptec Technologies Corp, Leica Geosystems Ag.

3. What are the main segments of the Europe LiDAR Industry?

The market segments include Product, Component, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Fast Paced Developments and Increasing Applications of Drones; Increasing Adoption in the Automotive Industry.

6. What are the notable trends driving market growth?

Engineering Industry to Hold Considerable Market Share.

7. Are there any restraints impacting market growth?

High Cost of the LiDAR Systems.

8. Can you provide examples of recent developments in the market?

June 2022 - Stellantis has selected Valeo's third-generation LiDAR to equip multiple models of its different automotive brands from 2024. The Valeo SCALA 3 LiDAR will enable these vehicles to be certified for level 3 automation. Valeo's third-generation LiDAR sees everything, even if it is far ahead and invisible to the human eye. It can detect objects more than 150 meters away that the human eye, cameras, and radars cannot, such as small objects with very low reflectivity.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe LiDAR Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe LiDAR Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe LiDAR Industry?

To stay informed about further developments, trends, and reports in the Europe LiDAR Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence