Key Insights

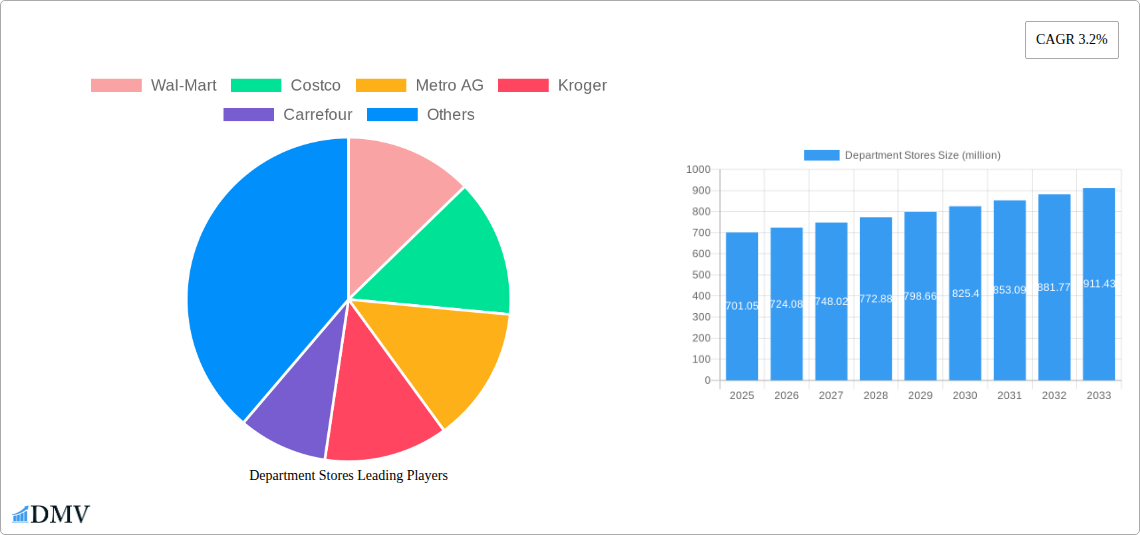

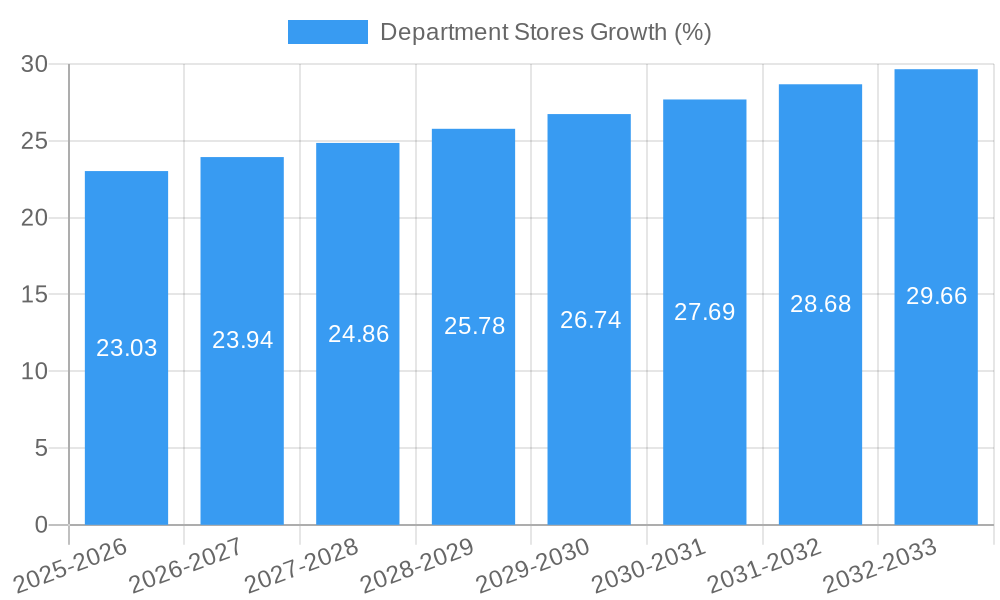

The global department store market, valued at $701.05 million in 2025, is projected to experience steady growth, driven by a Compound Annual Growth Rate (CAGR) of 3.2% from 2025 to 2033. This growth is fueled by several key factors. The increasing preference for experiential retail, where consumers seek more than just a transaction, is pushing department stores to innovate and offer engaging in-store experiences, including personalized services, events, and curated product selections. E-commerce integration is another significant driver, with established players like Walmart and Macy’s successfully blending online and offline channels to cater to evolving consumer preferences. Furthermore, strategic partnerships with luxury brands and the introduction of exclusive lines are enhancing the appeal and perceived value of department stores. However, the market faces challenges, primarily from the continuing rise of fast fashion and e-commerce giants offering competitive pricing and broader selections. Maintaining profitability amidst rising operational costs and competition requires a focus on operational efficiency, targeted marketing, and a commitment to providing unique and valuable customer experiences that differentiate them from online alternatives.

The competitive landscape is dominated by established players such as Walmart, Costco, and Carrefour, alongside regional giants like Yonghui Superstores and Bailian Group. These companies are strategically adapting their business models to navigate the evolving retail landscape. This includes investing in omnichannel strategies, focusing on private label brands to improve margins, and implementing advanced data analytics to better understand consumer behavior and personalize offerings. The success of these strategies will be crucial in determining the future trajectory of the department store market. The continued expansion into emerging markets, particularly in Asia, presents significant growth opportunities, while addressing challenges related to maintaining supply chains and adapting to local consumer preferences will be key to unlocking this potential. The next decade will likely see a consolidation in the market, with stronger players acquiring smaller chains or merging to achieve greater economies of scale and enhance their market positioning.

Department Stores Market: A Comprehensive Report (2019-2033)

This insightful report provides a comprehensive analysis of the global department stores market, encompassing market size, trends, leading players, and future projections. Valued at $XX million in 2024, the market is poised for significant growth, reaching an estimated $XX million by 2025 and projected to exceed $XX million by 2033. This in-depth study covers the period from 2019 to 2033, with a focus on the 2025-2033 forecast period. The report offers invaluable insights for stakeholders, investors, and industry professionals seeking to navigate the evolving landscape of the department store sector.

Department Stores Market Composition & Trends

This section delves into the intricate composition of the department store market, analyzing its concentration, innovation drivers, regulatory dynamics, substitute products, and end-user profiles. We also examine the significant impact of mergers and acquisitions (M&A) activities, providing a detailed overview of recent deals and their implications for market share distribution.

- Market Concentration: The global department store market exhibits a moderately concentrated structure, with key players like Wal-Mart, Costco, and Carrefour holding significant market share. However, regional variations exist, with some markets characterized by higher fragmentation.

- Innovation Catalysts: E-commerce integration, personalized shopping experiences, and the adoption of omnichannel strategies are key drivers of innovation, reshaping the traditional department store model.

- Regulatory Landscape: Regulations pertaining to labor practices, environmental sustainability, and data privacy significantly influence operational costs and strategies for department stores. Varying regulations across regions create diverse operational landscapes.

- Substitute Products: The rise of online marketplaces, specialty retailers, and discount stores presents significant competition, forcing department stores to adapt and differentiate their offerings.

- End-User Profiles: The target demographic for department stores is evolving, with a focus on diverse age groups and evolving consumption patterns. Understanding these segments is crucial for effective marketing and product development.

- M&A Activities: The department store industry has witnessed a flurry of M&A activity in recent years, with deal values exceeding $XX million in the period 2019-2024. These activities reflect strategic moves to expand market reach, optimize operations, and enhance brand portfolios. For example, the merger between [mention a specific example if available, otherwise state "a major player and a regional chain" ] led to significant changes in market share distribution.

Department Stores Industry Evolution

This section explores the transformative journey of the department store industry, tracing its growth trajectory, technological advancements, and the dynamic shifts in consumer preferences from 2019 to 2033. We examine the impact of technological disruptions on operational efficiency, customer engagement, and overall market growth.

The department store sector has witnessed significant evolution over the past decade, navigating challenges such as the rise of e-commerce and evolving consumer expectations. The market has experienced an average annual growth rate (AAGR) of X% during the historical period (2019-2024) and is projected to maintain an AAGR of Y% during the forecast period (2025-2033). This growth is largely driven by factors such as the increasing adoption of omni-channel strategies, personalized shopping experiences and the integration of advanced technologies like AI and Big Data to enhance operational efficiency and improve customer experience. The penetration of online shopping has rapidly increased, with an adoption rate of Z% in 2024, pushing traditional retailers to adapt and offer seamless omnichannel experiences.

Leading Regions, Countries, or Segments in Department Stores

This section identifies the leading regions, countries, or segments within the department store market, providing a granular analysis of the factors driving their dominance.

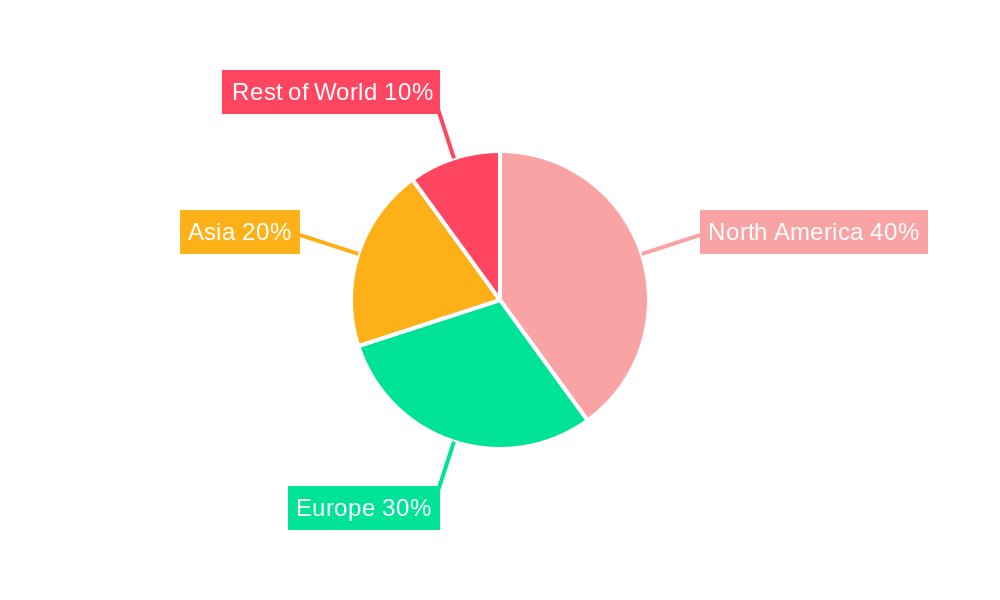

Dominant Region/Country: [Specify dominant region/country based on available data. E.g., North America currently holds the largest market share, driven by factors such as…]

- Key Drivers:

- High consumer spending power.

- Established retail infrastructure.

- Strong presence of major department store chains.

- Favorable regulatory environment.

- Key Drivers:

Dominant Segment: [Specify dominant segment if available, e.g., apparel and accessories].

- Key Drivers:

- Higher profit margins.

- Strong demand.

- Successful integration with online platforms.

- Key Drivers:

[Provide a paragraph further elaborating on the specific factors contributing to the dominance of the identified region/country/segment. Include details like investment trends, infrastructure development, and consumer behavior.]

Department Stores Product Innovations

Department stores are increasingly focusing on curated selections, private labels, and experiential retail to differentiate themselves. Technological advancements, such as personalized recommendations, virtual try-on tools, and mobile payment options, enhance the customer journey. The integration of data analytics and AI allows for more effective inventory management and targeted marketing campaigns, maximizing profitability and customer satisfaction. These innovations enhance the customer experience, increase sales conversion rates, and strengthen brand loyalty.

Propelling Factors for Department Stores Growth

Several key factors are driving the growth of the department store market. Technological advancements such as AI-driven personalization and enhanced e-commerce capabilities are improving customer experience and operational efficiency. Favorable economic conditions in key markets are boosting consumer spending, supporting industry growth. Government initiatives promoting retail development and investment in infrastructure further contribute to the expansion of the department store sector.

Obstacles in the Department Stores Market

The department store market faces several significant challenges. Increasing competition from e-commerce giants and specialized retailers is putting pressure on market share and profit margins. Supply chain disruptions, such as those caused by global events, can lead to significant delays and increased costs. Stringent regulatory requirements related to labor, environmental sustainability, and data privacy add operational complexities. These challenges require innovative strategies and robust risk management plans to mitigate their negative impact on profitability and market share.

Future Opportunities in Department Stores

The future of department stores lies in leveraging technology for enhanced customer engagement and operational efficiencies. The rise of experiential retail, offering unique and immersive shopping experiences, presents a significant opportunity. Expansion into new and emerging markets with high growth potential can drive market share growth. Focusing on sustainability and ethical sourcing can also attract environmentally conscious consumers, enhancing brand reputation and customer loyalty.

Major Players in the Department Stores Ecosystem

- Wal-Mart

- Costco

- Metro AG

- Kroger

- Carrefour

- Target

- Macy's

- Sears

- Kohl's

- Nordstrom

- JCPenney

- CR Vanguard

- RT-MART

- BHG

- Bailian Group

- Yonghui Superstores

- Trust-Mart

Key Developments in Department Stores Industry

- 2022-Q4: [Example: Launch of a new loyalty program by a major department store chain, impacting customer retention rates.]

- 2023-Q1: [Example: A significant merger between two regional department store chains, resulting in a reshaped market landscape.]

- 2024-Q2: [Example: Introduction of a new sustainable apparel line by a prominent department store, influencing consumer preferences.]

- [Add further bullet points with specific examples of relevant developments]

Strategic Department Stores Market Forecast

The department store market is projected to experience robust growth driven by several factors. The increasing adoption of omni-channel strategies, personalized shopping experiences, and technological advancements will enhance customer engagement and boost sales. Expansion into new markets and strategic partnerships will further contribute to market expansion. However, competition and macroeconomic factors need to be carefully considered. The forecast indicates a positive outlook, with significant potential for growth and innovation within the department store sector in the coming years.

Department Stores Segmentation

-

1. Application

- 1.1. Clothing and Footwear

- 1.2. Home and Kitchen Appliances

- 1.3. Bags, Wallets and Luggage

- 1.4. Watches and Jewelry

- 1.5. Cosmetics and Fragrances

- 1.6. Toys

- 1.7. Others

-

2. Type

- 2.1. Large Size

- 2.2. Small Size

Department Stores Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Department Stores REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 3.2% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Department Stores Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Clothing and Footwear

- 5.1.2. Home and Kitchen Appliances

- 5.1.3. Bags, Wallets and Luggage

- 5.1.4. Watches and Jewelry

- 5.1.5. Cosmetics and Fragrances

- 5.1.6. Toys

- 5.1.7. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Large Size

- 5.2.2. Small Size

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Department Stores Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Clothing and Footwear

- 6.1.2. Home and Kitchen Appliances

- 6.1.3. Bags, Wallets and Luggage

- 6.1.4. Watches and Jewelry

- 6.1.5. Cosmetics and Fragrances

- 6.1.6. Toys

- 6.1.7. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Large Size

- 6.2.2. Small Size

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Department Stores Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Clothing and Footwear

- 7.1.2. Home and Kitchen Appliances

- 7.1.3. Bags, Wallets and Luggage

- 7.1.4. Watches and Jewelry

- 7.1.5. Cosmetics and Fragrances

- 7.1.6. Toys

- 7.1.7. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Large Size

- 7.2.2. Small Size

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Department Stores Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Clothing and Footwear

- 8.1.2. Home and Kitchen Appliances

- 8.1.3. Bags, Wallets and Luggage

- 8.1.4. Watches and Jewelry

- 8.1.5. Cosmetics and Fragrances

- 8.1.6. Toys

- 8.1.7. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Large Size

- 8.2.2. Small Size

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Department Stores Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Clothing and Footwear

- 9.1.2. Home and Kitchen Appliances

- 9.1.3. Bags, Wallets and Luggage

- 9.1.4. Watches and Jewelry

- 9.1.5. Cosmetics and Fragrances

- 9.1.6. Toys

- 9.1.7. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Large Size

- 9.2.2. Small Size

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Department Stores Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Clothing and Footwear

- 10.1.2. Home and Kitchen Appliances

- 10.1.3. Bags, Wallets and Luggage

- 10.1.4. Watches and Jewelry

- 10.1.5. Cosmetics and Fragrances

- 10.1.6. Toys

- 10.1.7. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Large Size

- 10.2.2. Small Size

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 Wal-Mart

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Costco

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Metro AG

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Kroger

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Carrefour

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Target

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Macy's

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Sears

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Kohl's

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Nordstrom

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 JCPenney

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 CR Vanguard

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 RT-MART

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 BHG

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Bailian Group

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Yonghui Superstores

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Trust-Mart

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.1 Wal-Mart

List of Figures

- Figure 1: Global Department Stores Revenue Breakdown (million, %) by Region 2024 & 2032

- Figure 2: North America Department Stores Revenue (million), by Application 2024 & 2032

- Figure 3: North America Department Stores Revenue Share (%), by Application 2024 & 2032

- Figure 4: North America Department Stores Revenue (million), by Type 2024 & 2032

- Figure 5: North America Department Stores Revenue Share (%), by Type 2024 & 2032

- Figure 6: North America Department Stores Revenue (million), by Country 2024 & 2032

- Figure 7: North America Department Stores Revenue Share (%), by Country 2024 & 2032

- Figure 8: South America Department Stores Revenue (million), by Application 2024 & 2032

- Figure 9: South America Department Stores Revenue Share (%), by Application 2024 & 2032

- Figure 10: South America Department Stores Revenue (million), by Type 2024 & 2032

- Figure 11: South America Department Stores Revenue Share (%), by Type 2024 & 2032

- Figure 12: South America Department Stores Revenue (million), by Country 2024 & 2032

- Figure 13: South America Department Stores Revenue Share (%), by Country 2024 & 2032

- Figure 14: Europe Department Stores Revenue (million), by Application 2024 & 2032

- Figure 15: Europe Department Stores Revenue Share (%), by Application 2024 & 2032

- Figure 16: Europe Department Stores Revenue (million), by Type 2024 & 2032

- Figure 17: Europe Department Stores Revenue Share (%), by Type 2024 & 2032

- Figure 18: Europe Department Stores Revenue (million), by Country 2024 & 2032

- Figure 19: Europe Department Stores Revenue Share (%), by Country 2024 & 2032

- Figure 20: Middle East & Africa Department Stores Revenue (million), by Application 2024 & 2032

- Figure 21: Middle East & Africa Department Stores Revenue Share (%), by Application 2024 & 2032

- Figure 22: Middle East & Africa Department Stores Revenue (million), by Type 2024 & 2032

- Figure 23: Middle East & Africa Department Stores Revenue Share (%), by Type 2024 & 2032

- Figure 24: Middle East & Africa Department Stores Revenue (million), by Country 2024 & 2032

- Figure 25: Middle East & Africa Department Stores Revenue Share (%), by Country 2024 & 2032

- Figure 26: Asia Pacific Department Stores Revenue (million), by Application 2024 & 2032

- Figure 27: Asia Pacific Department Stores Revenue Share (%), by Application 2024 & 2032

- Figure 28: Asia Pacific Department Stores Revenue (million), by Type 2024 & 2032

- Figure 29: Asia Pacific Department Stores Revenue Share (%), by Type 2024 & 2032

- Figure 30: Asia Pacific Department Stores Revenue (million), by Country 2024 & 2032

- Figure 31: Asia Pacific Department Stores Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Department Stores Revenue million Forecast, by Region 2019 & 2032

- Table 2: Global Department Stores Revenue million Forecast, by Application 2019 & 2032

- Table 3: Global Department Stores Revenue million Forecast, by Type 2019 & 2032

- Table 4: Global Department Stores Revenue million Forecast, by Region 2019 & 2032

- Table 5: Global Department Stores Revenue million Forecast, by Application 2019 & 2032

- Table 6: Global Department Stores Revenue million Forecast, by Type 2019 & 2032

- Table 7: Global Department Stores Revenue million Forecast, by Country 2019 & 2032

- Table 8: United States Department Stores Revenue (million) Forecast, by Application 2019 & 2032

- Table 9: Canada Department Stores Revenue (million) Forecast, by Application 2019 & 2032

- Table 10: Mexico Department Stores Revenue (million) Forecast, by Application 2019 & 2032

- Table 11: Global Department Stores Revenue million Forecast, by Application 2019 & 2032

- Table 12: Global Department Stores Revenue million Forecast, by Type 2019 & 2032

- Table 13: Global Department Stores Revenue million Forecast, by Country 2019 & 2032

- Table 14: Brazil Department Stores Revenue (million) Forecast, by Application 2019 & 2032

- Table 15: Argentina Department Stores Revenue (million) Forecast, by Application 2019 & 2032

- Table 16: Rest of South America Department Stores Revenue (million) Forecast, by Application 2019 & 2032

- Table 17: Global Department Stores Revenue million Forecast, by Application 2019 & 2032

- Table 18: Global Department Stores Revenue million Forecast, by Type 2019 & 2032

- Table 19: Global Department Stores Revenue million Forecast, by Country 2019 & 2032

- Table 20: United Kingdom Department Stores Revenue (million) Forecast, by Application 2019 & 2032

- Table 21: Germany Department Stores Revenue (million) Forecast, by Application 2019 & 2032

- Table 22: France Department Stores Revenue (million) Forecast, by Application 2019 & 2032

- Table 23: Italy Department Stores Revenue (million) Forecast, by Application 2019 & 2032

- Table 24: Spain Department Stores Revenue (million) Forecast, by Application 2019 & 2032

- Table 25: Russia Department Stores Revenue (million) Forecast, by Application 2019 & 2032

- Table 26: Benelux Department Stores Revenue (million) Forecast, by Application 2019 & 2032

- Table 27: Nordics Department Stores Revenue (million) Forecast, by Application 2019 & 2032

- Table 28: Rest of Europe Department Stores Revenue (million) Forecast, by Application 2019 & 2032

- Table 29: Global Department Stores Revenue million Forecast, by Application 2019 & 2032

- Table 30: Global Department Stores Revenue million Forecast, by Type 2019 & 2032

- Table 31: Global Department Stores Revenue million Forecast, by Country 2019 & 2032

- Table 32: Turkey Department Stores Revenue (million) Forecast, by Application 2019 & 2032

- Table 33: Israel Department Stores Revenue (million) Forecast, by Application 2019 & 2032

- Table 34: GCC Department Stores Revenue (million) Forecast, by Application 2019 & 2032

- Table 35: North Africa Department Stores Revenue (million) Forecast, by Application 2019 & 2032

- Table 36: South Africa Department Stores Revenue (million) Forecast, by Application 2019 & 2032

- Table 37: Rest of Middle East & Africa Department Stores Revenue (million) Forecast, by Application 2019 & 2032

- Table 38: Global Department Stores Revenue million Forecast, by Application 2019 & 2032

- Table 39: Global Department Stores Revenue million Forecast, by Type 2019 & 2032

- Table 40: Global Department Stores Revenue million Forecast, by Country 2019 & 2032

- Table 41: China Department Stores Revenue (million) Forecast, by Application 2019 & 2032

- Table 42: India Department Stores Revenue (million) Forecast, by Application 2019 & 2032

- Table 43: Japan Department Stores Revenue (million) Forecast, by Application 2019 & 2032

- Table 44: South Korea Department Stores Revenue (million) Forecast, by Application 2019 & 2032

- Table 45: ASEAN Department Stores Revenue (million) Forecast, by Application 2019 & 2032

- Table 46: Oceania Department Stores Revenue (million) Forecast, by Application 2019 & 2032

- Table 47: Rest of Asia Pacific Department Stores Revenue (million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Department Stores?

The projected CAGR is approximately 3.2%.

2. Which companies are prominent players in the Department Stores?

Key companies in the market include Wal-Mart, Costco, Metro AG, Kroger, Carrefour, Target, Macy's, Sears, Kohl's, Nordstrom, JCPenney, CR Vanguard, RT-MART, BHG, Bailian Group, Yonghui Superstores, Trust-Mart.

3. What are the main segments of the Department Stores?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 701050 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Department Stores," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Department Stores report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Department Stores?

To stay informed about further developments, trends, and reports in the Department Stores, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence