Key Insights

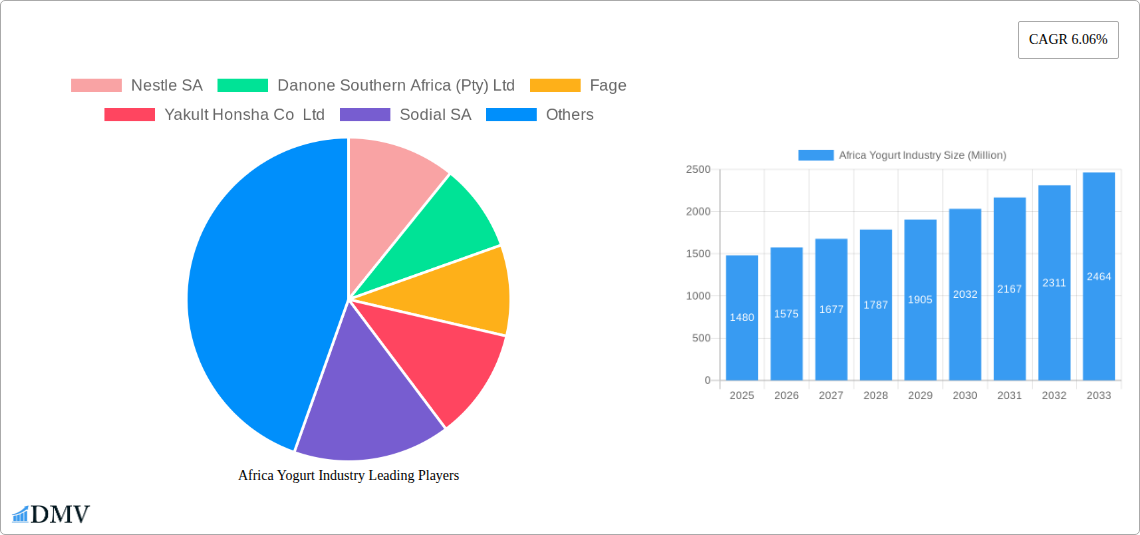

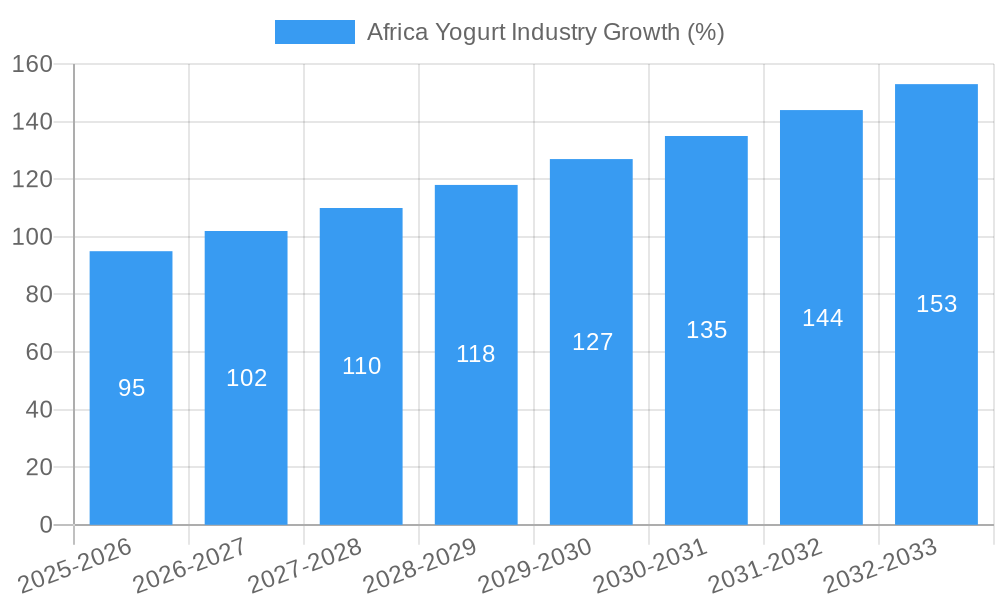

The African yogurt market, valued at $1.48 billion in 2025, is projected to experience robust growth, with a Compound Annual Growth Rate (CAGR) of 6.06% from 2025 to 2033. This expansion is driven by several key factors. Rising disposable incomes across various African nations are fueling increased consumer spending on convenient and nutritious food products like yogurt. The growing health-consciousness among consumers, particularly in urban areas, is also contributing significantly to market growth. Demand for dairy-based yogurts remains dominant, but the non-dairy segment is witnessing a notable upswing, driven by increasing awareness of lactose intolerance and the rise of veganism. Further driving growth are the expanding distribution channels, with supermarkets and hypermarkets leading the way, followed by a gradual increase in online sales. However, challenges remain, such as inconsistent infrastructure in certain regions, limited cold-chain logistics affecting product quality, and price sensitivity amongst consumers in some markets. The competitive landscape is relatively diverse, featuring both international players like Nestle and Danone, alongside regional and local brands catering to specific preferences. Market segmentation shows a strong preference for flavored yogurts, reflecting consumers' penchant for taste and variety.

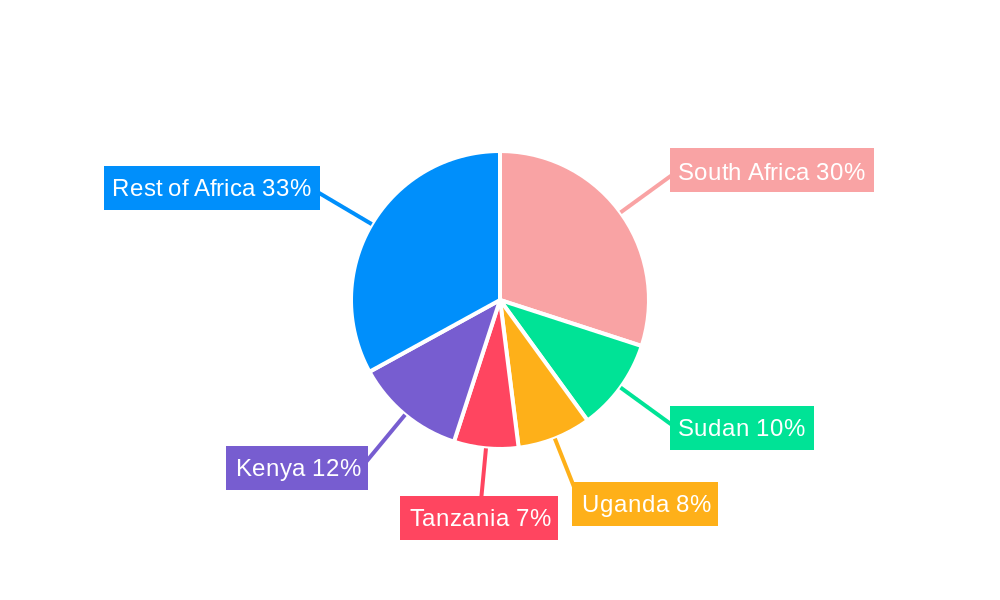

The forecast for 2026 to 2033 shows continued expansion, albeit with potential variations in growth depending on macroeconomic factors and successful adaptation by companies to overcome infrastructural and logistical challenges. South Africa, Sudan, Uganda, Tanzania, and Kenya represent key markets, with significant growth potential in the "Rest of Africa" segment. The market's success hinges on overcoming logistical hurdles, fostering greater product accessibility, and tailoring product offerings to suit the diverse cultural preferences and income levels within the African continent. Strategic partnerships between multinational corporations and local businesses could facilitate this expansion and unlock the significant potential of the African yogurt market. Innovation in product development, including new flavors and functional yogurts, will also play a crucial role in maintaining the impressive growth trajectory.

Africa Yogurt Industry: A Comprehensive Market Report (2019-2033)

This insightful report provides a detailed analysis of the dynamic Africa yogurt industry, offering a comprehensive overview of its market composition, evolution, leading players, and future prospects. The study period covers 2019-2033, with 2025 as the base and estimated year, and the forecast period spanning 2025-2033. This report is essential for stakeholders seeking to understand the industry's current landscape and capitalize on future growth opportunities. The African yogurt market, valued at xx Million in 2024, is poised for significant expansion, driven by factors such as rising disposable incomes, increasing health consciousness, and product innovation.

Africa Yogurt Industry Market Composition & Trends

This section delves into the competitive landscape of the African yogurt market, analyzing market concentration, innovation drivers, regulatory frameworks, substitute products, consumer profiles, and merger & acquisition (M&A) activities. The market is characterized by a mix of established international players and local producers.

- Market Share Distribution: Nestle SA holds an estimated xx% market share, followed by Danone Southern Africa (Pty) Ltd with xx%, and other key players like Fage, Yakult Honsha Co Ltd, and Viju Industries Nigeria Limited holding smaller, but significant shares. The remaining xx% is distributed among numerous smaller regional and local brands.

- Innovation Catalysts: Increasing consumer demand for healthier options, including low-sugar, high-protein, and plant-based yogurts, is a major catalyst for innovation. The introduction of novel flavors and functional ingredients is also shaping market trends.

- Regulatory Landscape: Varying regulatory standards across African nations influence product formulation and labeling, impacting market entry and competitiveness. A detailed analysis of these regulations is presented in the full report.

- Substitute Products: Competition comes from other dairy and non-dairy alternatives, including milk, fruit juices, and plant-based beverages. The report quantifies the competitive pressure from these substitutes.

- End-User Profiles: The report segments consumers based on demographics, dietary preferences, and purchasing behavior, highlighting key target segments for yogurt producers.

- M&A Activities: The report tracks recent M&A activities in the African yogurt market. While precise deal values are often confidential, the report analyzes the strategic implications of observed acquisitions and mergers, noting their impact on market consolidation and innovation. For example, a potential acquisition of a local brand by a multinational could be valued at xx Million, leading to increased market share and distribution network.

Africa Yogurt Industry Industry Evolution

This section analyzes the historical and projected growth trajectories of the African yogurt market, examining technological advancements, evolving consumer preferences, and the impact of macroeconomic factors. The market has experienced a Compound Annual Growth Rate (CAGR) of xx% during the historical period (2019-2024), driven by factors such as rising urbanization, increased disposable incomes, and a growing preference for convenient and healthy food options. Technological advancements, including improved production processes and extended shelf-life technologies, have also contributed to market expansion. Changing consumer preferences towards healthier and more functional foods are influencing product innovation and market segmentation, leading to the emergence of new product categories like non-dairy yogurt and high-protein yogurt. The report further predicts a CAGR of xx% during the forecast period (2025-2033), with specific growth rates detailed for each segment. The adoption of new packaging technologies, such as recyclable and sustainable packaging, is increasing and expected to further drive market growth. Specific examples of technological advancements and their market adoption rates are included.

Leading Regions, Countries, or Segments in Africa Yogurt Industry

This section identifies the dominant regions, countries, and segments within the African yogurt market.

- By Category: Dairy-based yogurt currently dominates the market, accounting for xx% of total sales. However, non-dairy yogurt is witnessing rapid growth, driven by increasing consumer demand for vegan and lactose-free options.

- By Type: Flavored yogurt constitutes the largest segment, driven by its appeal to a broader consumer base, particularly among younger demographics. Plain yogurt, while holding a significant share, is showing comparatively slower growth.

- By Distribution Channel: Supermarkets/hypermarkets are the primary distribution channel, benefiting from wide reach and established infrastructure. However, convenience stores and online channels are emerging as significant growth areas, particularly in urban centers.

Key Drivers:

- Investment Trends: Increased foreign direct investment (FDI) in the food processing sector is supporting the expansion of production capacity and distribution networks.

- Regulatory Support: Government initiatives promoting food security and agricultural development are creating a favorable environment for the growth of the yogurt industry.

The dominance of specific regions and countries is attributed to factors such as higher per capita income, greater access to refrigeration facilities, and the prevalence of Western dietary habits. For example, South Africa and Nigeria are leading markets due to their larger populations and comparatively higher per capita consumption of yogurt compared to other African nations.

Africa Yogurt Industry Product Innovations

Recent innovations in the African yogurt market include the introduction of new flavors (such as zero-sugar options from Chobani), unique blends (like General Mills' Yoplait Skittles), and high-protein varieties (General Mills' Ratio: Protein). These innovations respond directly to evolving consumer preferences, focusing on health, convenience, and diverse taste profiles. Technological advancements such as improved preservation methods and innovative packaging solutions are extending shelf life and enhancing product appeal. These innovations are enabling companies to command premium prices and gain a competitive advantage.

Propelling Factors for Africa Yogurt Industry Growth

Several factors are driving the growth of the African yogurt industry. Increasing urbanization leads to higher disposable incomes and a shift in consumer lifestyles favoring convenient and ready-to-eat foods. The rising awareness of health and wellness benefits associated with yogurt consumption is also driving demand. Government initiatives supporting agricultural development and food processing are creating a conducive business environment. Furthermore, the expanding retail infrastructure is improving product accessibility.

Obstacles in the Africa Yogurt Industry Market

Challenges include inconsistent power supply hindering production and storage, inadequate cold-chain infrastructure limiting distribution, particularly in rural areas, and the high cost of raw materials like milk, impacting production costs. The fragmented regulatory landscape across different African countries also creates complexities for manufacturers. Intense competition from both international and local players also places pressure on profit margins.

Future Opportunities in Africa Yogurt Industry

Future opportunities lie in tapping into the growing demand for functional yogurts (e.g., probiotics), expanding into underserved markets in rural areas, leveraging e-commerce platforms for wider reach, and focusing on sustainable and ethically sourced ingredients. Developing innovative packaging solutions addressing the challenges of heat and storage will significantly influence market growth.

Major Players in the Africa Yogurt Industry Ecosystem

- Nestle SA (Nestle SA)

- Danone Southern Africa (Pty) Ltd (Danone)

- Fage

- Yakult Honsha Co Ltd (Yakult Honsha)

- Sodial SA

- Parmalat Canada (Parmalat)

- Kraft foods group Inc (Kraft Heinz)

- Viju Industries Nigeria Limited

- General Mills (General Mills)

- Chobani Inc (Chobani)

Key Developments in Africa Yogurt Industry Industry

- April 2021: General Mills launched Ratio: Protein yogurt, focusing on high protein content.

- June 2021: General Mills and Mars Inc. launched Yoplait Skittles yogurt, a limited-edition product.

- 2021: Chobani LLC introduced new zero-sugar yogurt flavors (Mixed Berry and Strawberry).

Strategic Africa Yogurt Industry Market Forecast

The African yogurt market is projected to experience robust growth driven by rising disposable incomes, expanding retail infrastructure, and increasing health consciousness. The focus on innovation, particularly in developing healthier and more convenient options, will be crucial for success. The market offers significant opportunities for both established players and emerging brands, particularly in untapped regions and through the adoption of innovative distribution channels. The demand for high-protein and non-dairy alternatives is likely to fuel substantial future growth.

Africa Yogurt Industry Segmentation

-

1. Category

- 1.1. Dairy-based Yogurt

- 1.2. Non-dairy-based Yogurt

-

2. Type

- 2.1. Plain Yogurt

- 2.2. Flavored Yogurt

-

3. Distribution Channel

- 3.1. Supermarkets/Hypermarkets

- 3.2. Convenience Stores

- 3.3. Specialty Stores

- 3.4. Online Stores

- 3.5. Other Distribution Channels

-

4. Geography

- 4.1. South Africa

- 4.2. Nigeria

- 4.3. Egypt

- 4.4. Rest of Africa

Africa Yogurt Industry Segmentation By Geography

- 1. South Africa

- 2. Nigeria

- 3. Egypt

- 4. Rest of Africa

Africa Yogurt Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 6.06% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1 Introduction of new flavors

- 3.2.2 formulations

- 3.2.3 and types of yogurt

- 3.2.4 including low-fat

- 3.2.5 Greek yogurt

- 3.2.6 and yogurt with added probiotics

- 3.2.7 caters to diverse consumer preferences.

- 3.3. Market Restrains

- 3.3.1 Inadequate infrastructure and logistical issues in some regions can hinder the efficient distribution of yogurt products

- 3.3.2 particularly in rural areas.

- 3.4. Market Trends

- 3.4.1 Growing demand for functional and fortified yogurt products with added health benefits

- 3.4.2 such as probiotics and reduced sugar content.

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Africa Yogurt Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Category

- 5.1.1. Dairy-based Yogurt

- 5.1.2. Non-dairy-based Yogurt

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Plain Yogurt

- 5.2.2. Flavored Yogurt

- 5.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.3.1. Supermarkets/Hypermarkets

- 5.3.2. Convenience Stores

- 5.3.3. Specialty Stores

- 5.3.4. Online Stores

- 5.3.5. Other Distribution Channels

- 5.4. Market Analysis, Insights and Forecast - by Geography

- 5.4.1. South Africa

- 5.4.2. Nigeria

- 5.4.3. Egypt

- 5.4.4. Rest of Africa

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. South Africa

- 5.5.2. Nigeria

- 5.5.3. Egypt

- 5.5.4. Rest of Africa

- 5.1. Market Analysis, Insights and Forecast - by Category

- 6. South Africa Africa Yogurt Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Category

- 6.1.1. Dairy-based Yogurt

- 6.1.2. Non-dairy-based Yogurt

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Plain Yogurt

- 6.2.2. Flavored Yogurt

- 6.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.3.1. Supermarkets/Hypermarkets

- 6.3.2. Convenience Stores

- 6.3.3. Specialty Stores

- 6.3.4. Online Stores

- 6.3.5. Other Distribution Channels

- 6.4. Market Analysis, Insights and Forecast - by Geography

- 6.4.1. South Africa

- 6.4.2. Nigeria

- 6.4.3. Egypt

- 6.4.4. Rest of Africa

- 6.1. Market Analysis, Insights and Forecast - by Category

- 7. Nigeria Africa Yogurt Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Category

- 7.1.1. Dairy-based Yogurt

- 7.1.2. Non-dairy-based Yogurt

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Plain Yogurt

- 7.2.2. Flavored Yogurt

- 7.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 7.3.1. Supermarkets/Hypermarkets

- 7.3.2. Convenience Stores

- 7.3.3. Specialty Stores

- 7.3.4. Online Stores

- 7.3.5. Other Distribution Channels

- 7.4. Market Analysis, Insights and Forecast - by Geography

- 7.4.1. South Africa

- 7.4.2. Nigeria

- 7.4.3. Egypt

- 7.4.4. Rest of Africa

- 7.1. Market Analysis, Insights and Forecast - by Category

- 8. Egypt Africa Yogurt Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Category

- 8.1.1. Dairy-based Yogurt

- 8.1.2. Non-dairy-based Yogurt

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Plain Yogurt

- 8.2.2. Flavored Yogurt

- 8.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 8.3.1. Supermarkets/Hypermarkets

- 8.3.2. Convenience Stores

- 8.3.3. Specialty Stores

- 8.3.4. Online Stores

- 8.3.5. Other Distribution Channels

- 8.4. Market Analysis, Insights and Forecast - by Geography

- 8.4.1. South Africa

- 8.4.2. Nigeria

- 8.4.3. Egypt

- 8.4.4. Rest of Africa

- 8.1. Market Analysis, Insights and Forecast - by Category

- 9. Rest of Africa Africa Yogurt Industry Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Category

- 9.1.1. Dairy-based Yogurt

- 9.1.2. Non-dairy-based Yogurt

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Plain Yogurt

- 9.2.2. Flavored Yogurt

- 9.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 9.3.1. Supermarkets/Hypermarkets

- 9.3.2. Convenience Stores

- 9.3.3. Specialty Stores

- 9.3.4. Online Stores

- 9.3.5. Other Distribution Channels

- 9.4. Market Analysis, Insights and Forecast - by Geography

- 9.4.1. South Africa

- 9.4.2. Nigeria

- 9.4.3. Egypt

- 9.4.4. Rest of Africa

- 9.1. Market Analysis, Insights and Forecast - by Category

- 10. South Africa Africa Yogurt Industry Analysis, Insights and Forecast, 2019-2031

- 11. Sudan Africa Yogurt Industry Analysis, Insights and Forecast, 2019-2031

- 12. Uganda Africa Yogurt Industry Analysis, Insights and Forecast, 2019-2031

- 13. Tanzania Africa Yogurt Industry Analysis, Insights and Forecast, 2019-2031

- 14. Kenya Africa Yogurt Industry Analysis, Insights and Forecast, 2019-2031

- 15. Rest of Africa Africa Yogurt Industry Analysis, Insights and Forecast, 2019-2031

- 16. Competitive Analysis

- 16.1. Market Share Analysis 2024

- 16.2. Company Profiles

- 16.2.1 Nestle SA

- 16.2.1.1. Overview

- 16.2.1.2. Products

- 16.2.1.3. SWOT Analysis

- 16.2.1.4. Recent Developments

- 16.2.1.5. Financials (Based on Availability)

- 16.2.2 Danone Southern Africa (Pty) Ltd

- 16.2.2.1. Overview

- 16.2.2.2. Products

- 16.2.2.3. SWOT Analysis

- 16.2.2.4. Recent Developments

- 16.2.2.5. Financials (Based on Availability)

- 16.2.3 Fage

- 16.2.3.1. Overview

- 16.2.3.2. Products

- 16.2.3.3. SWOT Analysis

- 16.2.3.4. Recent Developments

- 16.2.3.5. Financials (Based on Availability)

- 16.2.4 Yakult Honsha Co Ltd

- 16.2.4.1. Overview

- 16.2.4.2. Products

- 16.2.4.3. SWOT Analysis

- 16.2.4.4. Recent Developments

- 16.2.4.5. Financials (Based on Availability)

- 16.2.5 Sodial SA

- 16.2.5.1. Overview

- 16.2.5.2. Products

- 16.2.5.3. SWOT Analysis

- 16.2.5.4. Recent Developments

- 16.2.5.5. Financials (Based on Availability)

- 16.2.6 Parmalat Canada

- 16.2.6.1. Overview

- 16.2.6.2. Products

- 16.2.6.3. SWOT Analysis

- 16.2.6.4. Recent Developments

- 16.2.6.5. Financials (Based on Availability)

- 16.2.7 Kraft foods group Inc

- 16.2.7.1. Overview

- 16.2.7.2. Products

- 16.2.7.3. SWOT Analysis

- 16.2.7.4. Recent Developments

- 16.2.7.5. Financials (Based on Availability)

- 16.2.8 Viju Industries Nigeria Limited

- 16.2.8.1. Overview

- 16.2.8.2. Products

- 16.2.8.3. SWOT Analysis

- 16.2.8.4. Recent Developments

- 16.2.8.5. Financials (Based on Availability)

- 16.2.9 General Mills

- 16.2.9.1. Overview

- 16.2.9.2. Products

- 16.2.9.3. SWOT Analysis

- 16.2.9.4. Recent Developments

- 16.2.9.5. Financials (Based on Availability)

- 16.2.10 Chobani Inc

- 16.2.10.1. Overview

- 16.2.10.2. Products

- 16.2.10.3. SWOT Analysis

- 16.2.10.4. Recent Developments

- 16.2.10.5. Financials (Based on Availability)

- 16.2.1 Nestle SA

List of Figures

- Figure 1: Africa Yogurt Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Africa Yogurt Industry Share (%) by Company 2024

List of Tables

- Table 1: Africa Yogurt Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Africa Yogurt Industry Revenue Million Forecast, by Category 2019 & 2032

- Table 3: Africa Yogurt Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 4: Africa Yogurt Industry Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 5: Africa Yogurt Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 6: Africa Yogurt Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 7: Africa Yogurt Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 8: South Africa Africa Yogurt Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Sudan Africa Yogurt Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Uganda Africa Yogurt Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: Tanzania Africa Yogurt Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: Kenya Africa Yogurt Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: Rest of Africa Africa Yogurt Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Africa Yogurt Industry Revenue Million Forecast, by Category 2019 & 2032

- Table 15: Africa Yogurt Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 16: Africa Yogurt Industry Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 17: Africa Yogurt Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 18: Africa Yogurt Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 19: Africa Yogurt Industry Revenue Million Forecast, by Category 2019 & 2032

- Table 20: Africa Yogurt Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 21: Africa Yogurt Industry Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 22: Africa Yogurt Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 23: Africa Yogurt Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 24: Africa Yogurt Industry Revenue Million Forecast, by Category 2019 & 2032

- Table 25: Africa Yogurt Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 26: Africa Yogurt Industry Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 27: Africa Yogurt Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 28: Africa Yogurt Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 29: Africa Yogurt Industry Revenue Million Forecast, by Category 2019 & 2032

- Table 30: Africa Yogurt Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 31: Africa Yogurt Industry Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 32: Africa Yogurt Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 33: Africa Yogurt Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Africa Yogurt Industry?

The projected CAGR is approximately 6.06%.

2. Which companies are prominent players in the Africa Yogurt Industry?

Key companies in the market include Nestle SA, Danone Southern Africa (Pty) Ltd, Fage, Yakult Honsha Co Ltd, Sodial SA, Parmalat Canada, Kraft foods group Inc, Viju Industries Nigeria Limited, General Mills, Chobani Inc.

3. What are the main segments of the Africa Yogurt Industry?

The market segments include Category, Type, Distribution Channel, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 1.48 Million as of 2022.

5. What are some drivers contributing to market growth?

Introduction of new flavors. formulations. and types of yogurt. including low-fat. Greek yogurt. and yogurt with added probiotics. caters to diverse consumer preferences..

6. What are the notable trends driving market growth?

Growing demand for functional and fortified yogurt products with added health benefits. such as probiotics and reduced sugar content..

7. Are there any restraints impacting market growth?

Inadequate infrastructure and logistical issues in some regions can hinder the efficient distribution of yogurt products. particularly in rural areas..

8. Can you provide examples of recent developments in the market?

In 2021, Chobani LLC launched new flavors of zero sugar yogurt. According to the company, these new flavors are Mixed Berry and Strawberry, respectively. The strategy behind the new launch and product innovation is to offer consumers a sugar-free product so that the company can target diabetic patients, and also this specific strategy will enable the company to expand the business and enlarge the company's product portfolio.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Africa Yogurt Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Africa Yogurt Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Africa Yogurt Industry?

To stay informed about further developments, trends, and reports in the Africa Yogurt Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence