Key Insights

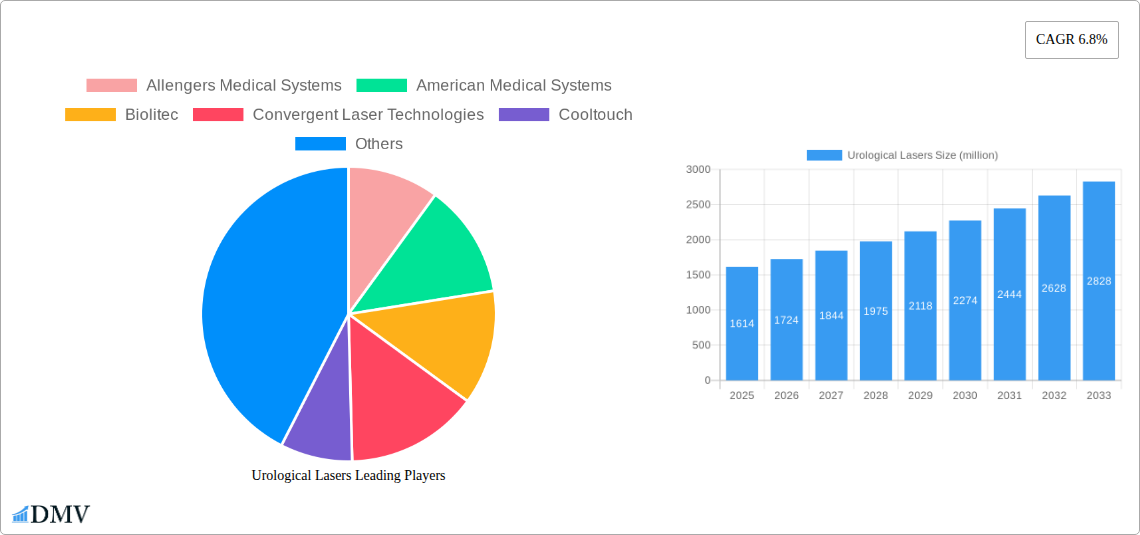

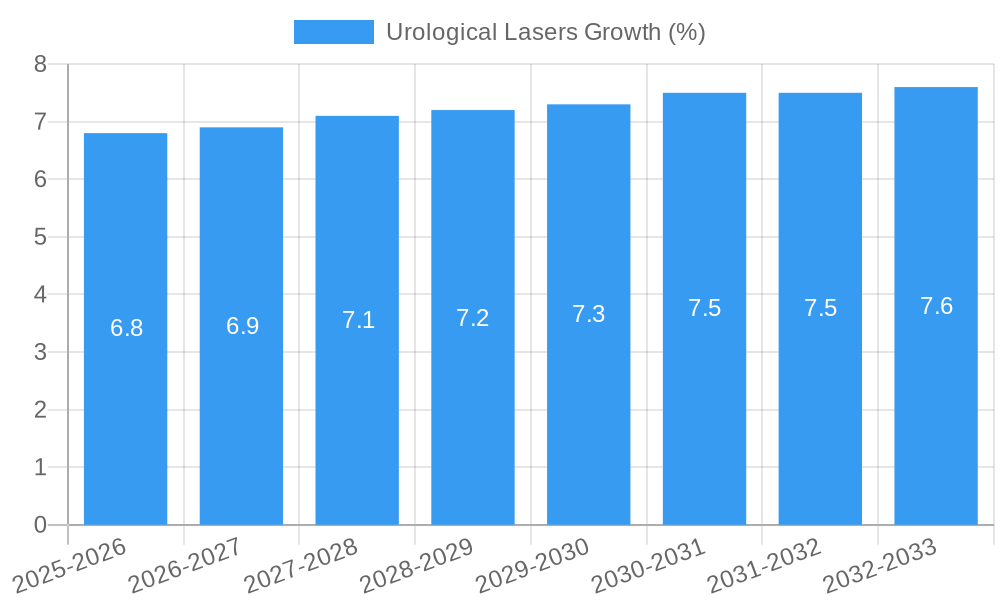

The global Urological Lasers market is poised for significant expansion, projected to reach an estimated value of approximately $1614 million by 2025. This growth trajectory is underpinned by a robust Compound Annual Growth Rate (CAGR) of 6.8% expected throughout the forecast period of 2025-2033. This expansion is primarily driven by the increasing prevalence of urological conditions such as kidney stones, benign prostatic hyperplasia (BPH), and various forms of cancer, necessitating minimally invasive and highly effective treatment options. The technological advancements in laser therapy, offering enhanced precision, reduced patient trauma, and faster recovery times, are key enablers of this market growth. Furthermore, a growing emphasis on outpatient procedures and the increasing adoption of advanced medical devices in healthcare facilities worldwide are contributing to the positive market sentiment. The market's dynamism is also fueled by continuous innovation from leading companies, leading to the development of more sophisticated and versatile urological laser systems.

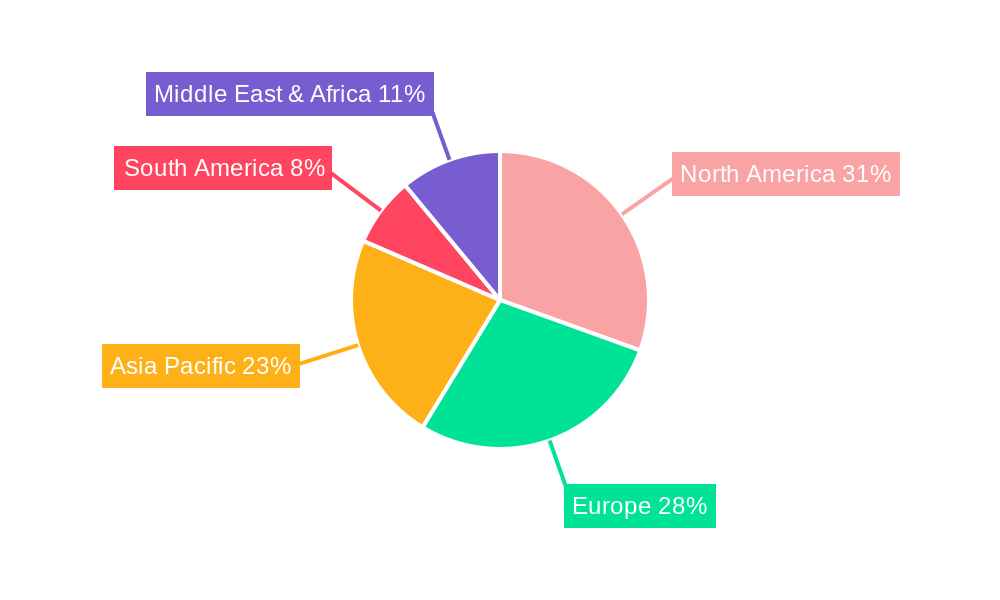

The market is segmented across various applications, with Hospitals emerging as the dominant segment due to their comprehensive infrastructure and higher patient volumes for complex procedures. Clinics also represent a significant and growing segment, reflecting the trend towards specialized urological care and the increasing affordability of laser technology for smaller healthcare providers. In terms of type, Holmium Lasers and Ho:YAG Lasers are expected to lead the market, owing to their established efficacy in lithotripsy and tissue ablation. The Asia Pacific region is anticipated to witness the fastest growth, propelled by rising healthcare expenditure, improving access to advanced medical technologies, and a large patient population. North America and Europe are expected to maintain substantial market shares, driven by early adoption of innovative technologies and well-established healthcare systems. However, factors such as high initial investment costs for advanced laser systems and the availability of alternative treatment modalities may present some restraints to the market's rapid expansion.

Here is the SEO-optimized and insightful report description for Urological Lasers:

Urological Lasers Market Composition & Trends

The Urological Lasers market is characterized by a dynamic interplay of innovation, evolving clinical practices, and increasing demand for minimally invasive treatment options. Market concentration is moderately fragmented, with key players like Olympus, Richard Wolf, and Quanta System holding significant shares. However, emerging companies such as Shanghai Raykeen and Biolitec are rapidly gaining traction, driven by advancements in laser technology and strategic market penetration. Innovation catalysts are primarily focused on developing higher-power, more precise, and user-friendly laser systems for a range of urological conditions, including BPH, kidney stones, and prostate cancer. The regulatory landscape, particularly stringent FDA and CE marking requirements, influences product development cycles and market entry strategies. Substitute products, such as traditional surgical instruments and alternative energy devices, continue to pose a competitive challenge, albeit with limitations in terms of precision and patient recovery times. End-user profiles are diverse, encompassing hospitals, specialized urology clinics, and ambulatory surgical centers, each with distinct purchasing criteria and adoption rates. Mergers and acquisitions (M&A) activities are pivotal in consolidating market share and acquiring cutting-edge technologies. For instance, past M&A deals have been valued in the range of fifty to one hundred million dollars, enabling larger entities to expand their product portfolios and geographical reach. The distribution of market share is expected to see shifts with the growing adoption of advanced laser modalities.

- Market Concentration: Moderately fragmented with a mix of established and emerging players.

- Innovation Catalysts: Development of high-power, precision-guided, and user-friendly laser systems.

- Regulatory Landscape: Influenced by FDA and CE marking, impacting product launch timelines.

- Substitute Products: Traditional surgical instruments and alternative energy devices.

- End-User Profiles: Hospitals, specialized urology clinics, ambulatory surgical centers.

- M&A Activities: Crucial for market consolidation and technology acquisition, with deal values ranging from fifty to one hundred million dollars.

Urological Lasers Industry Evolution

The urological lasers industry has witnessed a remarkable evolution throughout the historical period of 2019–2024, driven by significant technological advancements and an increasing emphasis on patient-centric, minimally invasive surgical techniques. The market has expanded from a nascent stage to a robust sector, with a projected Compound Annual Growth Rate (CAGR) of approximately 6.5% from the base year of 2025 to the forecast period ending in 2033. This growth trajectory is underpinned by a sustained rise in the prevalence of urological diseases, including benign prostatic hyperplasia (BPH), kidney stones (urolithiasis), and prostate cancer, necessitating more effective and less traumatic treatment modalities. The adoption of laser technologies, particularly Holmium Laser (Ho:YAG Laser) and Thulium Laser, has surged due to their superior tissue ablation capabilities, minimal collateral damage, and faster patient recovery times compared to conventional surgical methods. For example, Ho:YAG lasers have become the gold standard for lithotripsy, offering fragmentation of stones of all compositions. Thulium lasers are increasingly being utilized for precise tissue vaporization and enucleation.

Technological advancements have focused on increasing laser power, improving beam delivery systems (e.g., flexible and semi-rigid ureteroscopes), and integrating advanced imaging and navigation capabilities. Innovations like pulsed fiber lasers and next-generation diode lasers are also contributing to market expansion by offering enhanced versatility and cost-effectiveness. Consumer demand has shifted considerably, with patients actively seeking treatments that minimize hospitalization, reduce pain, and lead to quicker return to daily activities. Healthcare providers, in response, are investing in advanced laser equipment to improve patient outcomes and enhance their service offerings. The industry has also seen the development of advanced software for precise energy delivery and treatment planning, further refining the efficacy of urological laser procedures. The market size, which was around 1,200 million in the historical period, is expected to reach an estimated 1,900 million by the end of the forecast period, demonstrating substantial market expansion. The estimated year of 2025 will be a pivotal point, with a market size projected at 1,400 million, reflecting continuous growth.

Leading Regions, Countries, or Segments in Urological Lasers

The urological lasers market is experiencing significant dominance and growth across various regions and segments, driven by a confluence of factors including advanced healthcare infrastructure, increasing disposable income, a high prevalence of urological diseases, and supportive government initiatives. North America, particularly the United States, consistently leads the market due to its early adoption of advanced medical technologies, robust research and development activities, and a strong presence of leading medical device manufacturers. The high rate of urological surgeries, coupled with an aging population susceptible to conditions like BPH, further fuels demand.

The Application segment of Hospitals represents the largest share within the urological lasers market. Hospitals, being primary healthcare providers with extensive surgical facilities and dedicated urology departments, are significant adopters of these advanced laser systems. The ability to perform complex procedures and manage a wide range of patient volumes makes them ideal environments for urological laser utilization. Clinics, particularly specialized urology centers, are also a rapidly growing segment, offering more focused and often more accessible treatment options.

Within the Type segment, Holmium Laser (Ho:YAG Laser) holds the most prominent position. Its unparalleled efficacy in stone fragmentation (lithotripsy) and its versatility in treating various stone compositions and sizes have made it indispensable in urological practice. The development of sophisticated delivery systems has further enhanced its utility in treating kidney stones and upper tract urothelial carcinoma. Thulium Laser is a fast-growing segment, gaining traction for its precise tissue vaporization capabilities, especially in the treatment of BPH (e.g., HoLEP – Holmium Laser Enucleation of the Prostate, ThuLEP – Thulium Laser Enucleation of the Prostate) and precise tumor ablation. The segment is projected to see accelerated growth due to ongoing technological refinements and increasing surgeon comfort with the modality. The market is projected to grow from approximately 1,200 million in the historical period to an estimated 1,900 million by the end of the forecast period (2033), with the base year 2025 anticipating a market size of 1,400 million.

- Dominant Region: North America, driven by technological adoption and disease prevalence.

- Leading Application Segment: Hospitals, due to comprehensive surgical infrastructure.

- Key Type Segment: Holmium Laser (Ho:YAG Laser), for its established lithotripsy and ablation capabilities.

- Fastest Growing Type Segment: Thulium Laser, due to advancements in BPH and tumor treatment.

- Investment Trends: Significant capital investment in advanced laser technology by healthcare institutions.

- Regulatory Support: Favorable regulatory environments in key markets facilitating product approval and adoption.

Urological Lasers Product Innovations

Recent product innovations in the urological lasers market are revolutionizing treatment protocols, offering enhanced precision and minimally invasive options. Companies are focusing on developing higher-power Holmium lasers (up to 200 watts) for more efficient stone dusting and fragmentation, alongside advanced fiber technologies that ensure superior durability and maneuverability. Innovations also include the integration of sophisticated imaging systems and real-time feedback mechanisms, allowing surgeons to visualize tissue interaction with unprecedented clarity and control. For instance, the development of ‘smart’ laser fibers that adapt to varying tissue densities and the introduction of pulsed laser modes are enhancing surgical outcomes and reducing thermal damage. These advancements translate into reduced operative times, lower complication rates, and faster patient recovery.

Propelling Factors for Urological Lasers Growth

The urological lasers market is propelled by several key factors that are shaping its growth trajectory. The increasing global prevalence of urological diseases, such as kidney stones, benign prostatic hyperplasia (BPH), and urological cancers, directly translates into a higher demand for effective treatment solutions. Technological advancements are at the forefront, with continuous innovation in laser power, precision, and portability leading to the development of more effective and minimally invasive procedures. The growing preference for minimally invasive surgeries among patients and healthcare providers, driven by benefits like reduced pain, shorter hospital stays, and faster recovery times, is a significant catalyst. Furthermore, favorable reimbursement policies and increasing healthcare expenditure in both developed and emerging economies are enhancing accessibility to these advanced treatment modalities.

- Rising Prevalence of Urological Diseases: Increasing incidence of kidney stones, BPH, and urological cancers.

- Technological Advancements: Innovations in laser power, precision, and fiber optics.

- Demand for Minimally Invasive Surgery: Patient and physician preference for less invasive procedures.

- Favorable Reimbursement Policies: Supportive insurance coverage for laser treatments.

- Growing Healthcare Expenditure: Increased investment in advanced medical technologies globally.

Obstacles in the Urological Lasers Market

Despite the robust growth, the urological lasers market faces several obstacles that can impede its expansion. The high initial cost of advanced urological laser systems poses a significant barrier to adoption, particularly for smaller clinics or healthcare facilities in low-income regions. Stringent regulatory approval processes in different countries can lead to extended product launch timelines and increased development costs. The availability of skilled surgeons trained in the use of these advanced laser technologies is also a constraint, requiring substantial investment in training and education. Furthermore, the presence of well-established alternative treatment modalities, including traditional surgical techniques and other energy-based devices, continues to exert competitive pressure. Supply chain disruptions, as experienced recently, can also impact the availability of critical components and finished products, leading to price volatility and potential delays.

- High Initial Investment Costs: Significant capital expenditure for advanced laser systems.

- Strict Regulatory Hurdles: Lengthy and complex approval processes across different geographies.

- Shortage of Skilled Surgeons: Need for specialized training and expertise in laser procedures.

- Competition from Alternative Treatments: Established traditional surgeries and other energy-based devices.

- Supply Chain Volatility: Potential disruptions affecting product availability and pricing.

Future Opportunities in Urological Lasers

The urological lasers market is ripe with future opportunities, driven by emerging technologies and unmet clinical needs. The development of miniaturized and portable laser systems presents a significant opportunity to enhance accessibility, particularly in remote areas or for point-of-care applications. Further advancements in artificial intelligence (AI) and machine learning integration with laser systems hold promise for optimizing treatment planning and delivering personalized therapies. The expanding healthcare infrastructure in emerging economies, coupled with increasing disposable incomes, creates new market frontiers for urological laser adoption. Moreover, the exploration of novel laser wavelengths and delivery mechanisms for treating a wider spectrum of urological conditions, including complex conditions and conditions currently managed with less effective methods, represents a substantial growth avenue. The increasing focus on outpatient procedures and same-day surgery further bolsters the demand for efficient and effective laser technologies.

- Miniaturization and Portability: Enabling wider accessibility and point-of-care applications.

- AI and Machine Learning Integration: Optimizing treatment planning and personalization.

- Emerging Markets Expansion: Tapping into growing healthcare sectors in developing economies.

- Novel Wavelengths and Delivery Systems: Expanding treatment capabilities for diverse urological conditions.

- Outpatient Surgery Trends: Catering to the demand for efficient, same-day procedures.

Major Players in the Urological Lasers Ecosystem

- Allengers Medical Systems

- American Medical Systems

- Biolitec

- Convergent Laser Technologies

- Cooltouch

- Deka

- EMS Electro Medical Systems

- Fisioline

- Hyper Photonics

- INTERmedic

- JenaSurgical

- Medency

- Olympus

- OmniGuide

- ProSurg

- Quanta System

- Richard Wolf

- Shanghai Raykeen

Key Developments in Urological Lasers Industry

- 2024 February: Launch of a new generation of high-power Holmium laser systems with enhanced fiber durability and maneuverability, significantly improving lithotripsy efficiency.

- 2023 October: A major manufacturer secured FDA approval for an advanced Thulium laser system for precise BPH treatment, leading to wider clinical adoption.

- 2023 May: Introduction of AI-powered laser treatment planning software, enabling personalized surgical approaches and improved outcomes.

- 2022 December: Acquisition of a promising laser technology startup by a leading medical device company, aimed at expanding their urological laser portfolio.

- 2022 September: Rollout of advanced flexible ureteroscopes designed for optimal interaction with Holmium lasers, enhancing access and visualization in complex stone cases.

- 2021 November: Significant investment by a European conglomerate in a facility dedicated to the research and development of next-generation urological laser technologies.

- 2021 April: A key player announced strategic partnerships to enhance the distribution network for their urological laser devices in Asia-Pacific markets.

Strategic Urological Lasers Market Forecast

The strategic forecast for the urological lasers market indicates a period of sustained and robust growth driven by an intensifying focus on patient outcomes and the increasing adoption of minimally invasive techniques. The continued evolution of Holmium and Thulium laser technologies, coupled with the exploration of new laser modalities, will unlock new therapeutic avenues and improve existing ones. The growing demand in emerging markets, fueled by improving healthcare infrastructure and rising disposable incomes, presents a significant opportunity for market expansion. Strategic collaborations between technology developers, healthcare providers, and regulatory bodies will be crucial in navigating the market dynamics and ensuring the widespread availability of these life-enhancing technologies. The market is poised for an upward trajectory, projecting an estimated market size of 1,900 million by 2033.

Urological Lasers Segmentation

-

1. Application

- 1.1. Hospital

- 1.2. Clinic

- 1.3. Others

-

2. Type

- 2.1. Holmium Laser

- 2.2. Ho:YAG Laser

- 2.3. Thulium Laser

- 2.4. Others

Urological Lasers Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Urological Lasers REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 6.8% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Urological Lasers Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Hospital

- 5.1.2. Clinic

- 5.1.3. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Holmium Laser

- 5.2.2. Ho:YAG Laser

- 5.2.3. Thulium Laser

- 5.2.4. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Urological Lasers Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Hospital

- 6.1.2. Clinic

- 6.1.3. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Holmium Laser

- 6.2.2. Ho:YAG Laser

- 6.2.3. Thulium Laser

- 6.2.4. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Urological Lasers Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Hospital

- 7.1.2. Clinic

- 7.1.3. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Holmium Laser

- 7.2.2. Ho:YAG Laser

- 7.2.3. Thulium Laser

- 7.2.4. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Urological Lasers Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Hospital

- 8.1.2. Clinic

- 8.1.3. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Holmium Laser

- 8.2.2. Ho:YAG Laser

- 8.2.3. Thulium Laser

- 8.2.4. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Urological Lasers Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Hospital

- 9.1.2. Clinic

- 9.1.3. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Holmium Laser

- 9.2.2. Ho:YAG Laser

- 9.2.3. Thulium Laser

- 9.2.4. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Urological Lasers Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Hospital

- 10.1.2. Clinic

- 10.1.3. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Holmium Laser

- 10.2.2. Ho:YAG Laser

- 10.2.3. Thulium Laser

- 10.2.4. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 Allengers Medical Systems

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 American Medical Systems

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Biolitec

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Convergent Laser Technologies

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Cooltouch

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Deka

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 EMS Electro Medical Systems

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Fisioline

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Hyper Photonics

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 INTERmedic

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 JenaSurgical

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Medency

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Olympus

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 OmniGuide

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 ProSurg

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Quanta System

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Richard Wolf

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 Shanghai Raykeen

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.1 Allengers Medical Systems

List of Figures

- Figure 1: Global Urological Lasers Revenue Breakdown (million, %) by Region 2024 & 2032

- Figure 2: North America Urological Lasers Revenue (million), by Application 2024 & 2032

- Figure 3: North America Urological Lasers Revenue Share (%), by Application 2024 & 2032

- Figure 4: North America Urological Lasers Revenue (million), by Type 2024 & 2032

- Figure 5: North America Urological Lasers Revenue Share (%), by Type 2024 & 2032

- Figure 6: North America Urological Lasers Revenue (million), by Country 2024 & 2032

- Figure 7: North America Urological Lasers Revenue Share (%), by Country 2024 & 2032

- Figure 8: South America Urological Lasers Revenue (million), by Application 2024 & 2032

- Figure 9: South America Urological Lasers Revenue Share (%), by Application 2024 & 2032

- Figure 10: South America Urological Lasers Revenue (million), by Type 2024 & 2032

- Figure 11: South America Urological Lasers Revenue Share (%), by Type 2024 & 2032

- Figure 12: South America Urological Lasers Revenue (million), by Country 2024 & 2032

- Figure 13: South America Urological Lasers Revenue Share (%), by Country 2024 & 2032

- Figure 14: Europe Urological Lasers Revenue (million), by Application 2024 & 2032

- Figure 15: Europe Urological Lasers Revenue Share (%), by Application 2024 & 2032

- Figure 16: Europe Urological Lasers Revenue (million), by Type 2024 & 2032

- Figure 17: Europe Urological Lasers Revenue Share (%), by Type 2024 & 2032

- Figure 18: Europe Urological Lasers Revenue (million), by Country 2024 & 2032

- Figure 19: Europe Urological Lasers Revenue Share (%), by Country 2024 & 2032

- Figure 20: Middle East & Africa Urological Lasers Revenue (million), by Application 2024 & 2032

- Figure 21: Middle East & Africa Urological Lasers Revenue Share (%), by Application 2024 & 2032

- Figure 22: Middle East & Africa Urological Lasers Revenue (million), by Type 2024 & 2032

- Figure 23: Middle East & Africa Urological Lasers Revenue Share (%), by Type 2024 & 2032

- Figure 24: Middle East & Africa Urological Lasers Revenue (million), by Country 2024 & 2032

- Figure 25: Middle East & Africa Urological Lasers Revenue Share (%), by Country 2024 & 2032

- Figure 26: Asia Pacific Urological Lasers Revenue (million), by Application 2024 & 2032

- Figure 27: Asia Pacific Urological Lasers Revenue Share (%), by Application 2024 & 2032

- Figure 28: Asia Pacific Urological Lasers Revenue (million), by Type 2024 & 2032

- Figure 29: Asia Pacific Urological Lasers Revenue Share (%), by Type 2024 & 2032

- Figure 30: Asia Pacific Urological Lasers Revenue (million), by Country 2024 & 2032

- Figure 31: Asia Pacific Urological Lasers Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Urological Lasers Revenue million Forecast, by Region 2019 & 2032

- Table 2: Global Urological Lasers Revenue million Forecast, by Application 2019 & 2032

- Table 3: Global Urological Lasers Revenue million Forecast, by Type 2019 & 2032

- Table 4: Global Urological Lasers Revenue million Forecast, by Region 2019 & 2032

- Table 5: Global Urological Lasers Revenue million Forecast, by Application 2019 & 2032

- Table 6: Global Urological Lasers Revenue million Forecast, by Type 2019 & 2032

- Table 7: Global Urological Lasers Revenue million Forecast, by Country 2019 & 2032

- Table 8: United States Urological Lasers Revenue (million) Forecast, by Application 2019 & 2032

- Table 9: Canada Urological Lasers Revenue (million) Forecast, by Application 2019 & 2032

- Table 10: Mexico Urological Lasers Revenue (million) Forecast, by Application 2019 & 2032

- Table 11: Global Urological Lasers Revenue million Forecast, by Application 2019 & 2032

- Table 12: Global Urological Lasers Revenue million Forecast, by Type 2019 & 2032

- Table 13: Global Urological Lasers Revenue million Forecast, by Country 2019 & 2032

- Table 14: Brazil Urological Lasers Revenue (million) Forecast, by Application 2019 & 2032

- Table 15: Argentina Urological Lasers Revenue (million) Forecast, by Application 2019 & 2032

- Table 16: Rest of South America Urological Lasers Revenue (million) Forecast, by Application 2019 & 2032

- Table 17: Global Urological Lasers Revenue million Forecast, by Application 2019 & 2032

- Table 18: Global Urological Lasers Revenue million Forecast, by Type 2019 & 2032

- Table 19: Global Urological Lasers Revenue million Forecast, by Country 2019 & 2032

- Table 20: United Kingdom Urological Lasers Revenue (million) Forecast, by Application 2019 & 2032

- Table 21: Germany Urological Lasers Revenue (million) Forecast, by Application 2019 & 2032

- Table 22: France Urological Lasers Revenue (million) Forecast, by Application 2019 & 2032

- Table 23: Italy Urological Lasers Revenue (million) Forecast, by Application 2019 & 2032

- Table 24: Spain Urological Lasers Revenue (million) Forecast, by Application 2019 & 2032

- Table 25: Russia Urological Lasers Revenue (million) Forecast, by Application 2019 & 2032

- Table 26: Benelux Urological Lasers Revenue (million) Forecast, by Application 2019 & 2032

- Table 27: Nordics Urological Lasers Revenue (million) Forecast, by Application 2019 & 2032

- Table 28: Rest of Europe Urological Lasers Revenue (million) Forecast, by Application 2019 & 2032

- Table 29: Global Urological Lasers Revenue million Forecast, by Application 2019 & 2032

- Table 30: Global Urological Lasers Revenue million Forecast, by Type 2019 & 2032

- Table 31: Global Urological Lasers Revenue million Forecast, by Country 2019 & 2032

- Table 32: Turkey Urological Lasers Revenue (million) Forecast, by Application 2019 & 2032

- Table 33: Israel Urological Lasers Revenue (million) Forecast, by Application 2019 & 2032

- Table 34: GCC Urological Lasers Revenue (million) Forecast, by Application 2019 & 2032

- Table 35: North Africa Urological Lasers Revenue (million) Forecast, by Application 2019 & 2032

- Table 36: South Africa Urological Lasers Revenue (million) Forecast, by Application 2019 & 2032

- Table 37: Rest of Middle East & Africa Urological Lasers Revenue (million) Forecast, by Application 2019 & 2032

- Table 38: Global Urological Lasers Revenue million Forecast, by Application 2019 & 2032

- Table 39: Global Urological Lasers Revenue million Forecast, by Type 2019 & 2032

- Table 40: Global Urological Lasers Revenue million Forecast, by Country 2019 & 2032

- Table 41: China Urological Lasers Revenue (million) Forecast, by Application 2019 & 2032

- Table 42: India Urological Lasers Revenue (million) Forecast, by Application 2019 & 2032

- Table 43: Japan Urological Lasers Revenue (million) Forecast, by Application 2019 & 2032

- Table 44: South Korea Urological Lasers Revenue (million) Forecast, by Application 2019 & 2032

- Table 45: ASEAN Urological Lasers Revenue (million) Forecast, by Application 2019 & 2032

- Table 46: Oceania Urological Lasers Revenue (million) Forecast, by Application 2019 & 2032

- Table 47: Rest of Asia Pacific Urological Lasers Revenue (million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Urological Lasers?

The projected CAGR is approximately 6.8%.

2. Which companies are prominent players in the Urological Lasers?

Key companies in the market include Allengers Medical Systems, American Medical Systems, Biolitec, Convergent Laser Technologies, Cooltouch, Deka, EMS Electro Medical Systems, Fisioline, Hyper Photonics, INTERmedic, JenaSurgical, Medency, Olympus, OmniGuide, ProSurg, Quanta System, Richard Wolf, Shanghai Raykeen.

3. What are the main segments of the Urological Lasers?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 1614 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Urological Lasers," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Urological Lasers report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Urological Lasers?

To stay informed about further developments, trends, and reports in the Urological Lasers, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence