Key Insights

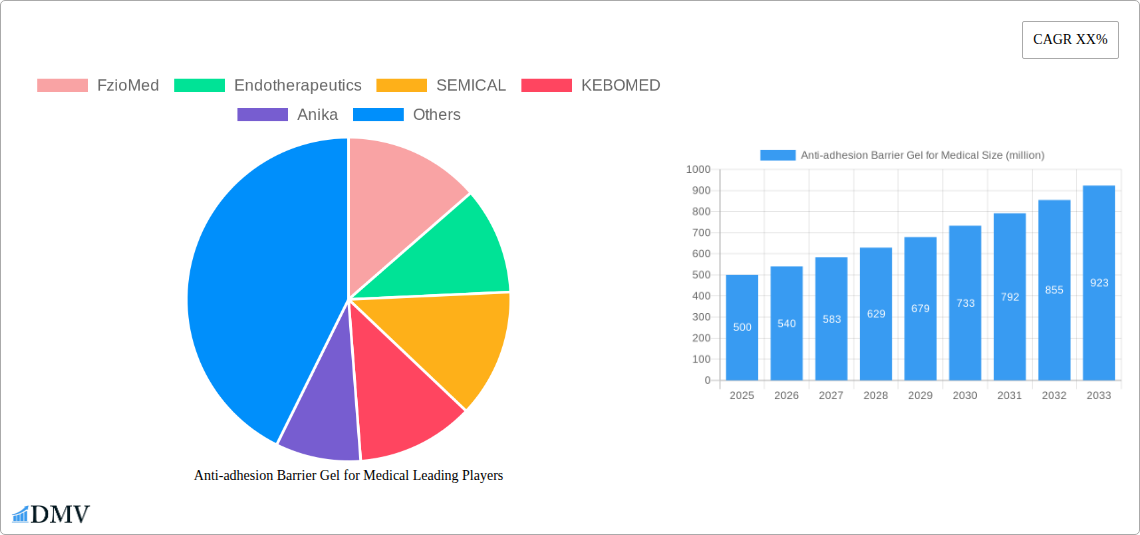

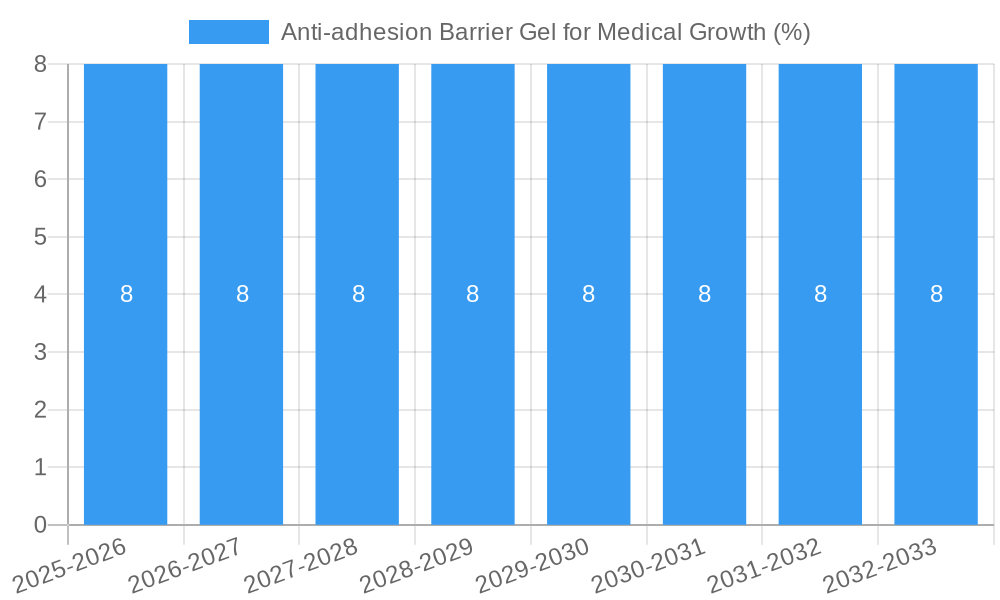

The global market for Anti-adhesion Barrier Gel is poised for significant expansion, driven by an increasing prevalence of surgical procedures and a growing awareness of their role in preventing post-operative complications. Valued at an estimated USD 500 million in 2025, the market is projected to witness a robust Compound Annual Growth Rate (CAGR) of 8%, reaching approximately USD 1.1 billion by 2033. This growth is primarily fueled by the rising demand in abdominal surgeries, gynecological procedures, and orthopedic interventions, where the formation of adhesions can lead to chronic pain, bowel obstruction, and infertility, necessitating effective preventative measures. The injectables type segment, offering precise application and superior efficacy, is expected to dominate the market, supported by advancements in formulation and delivery technologies.

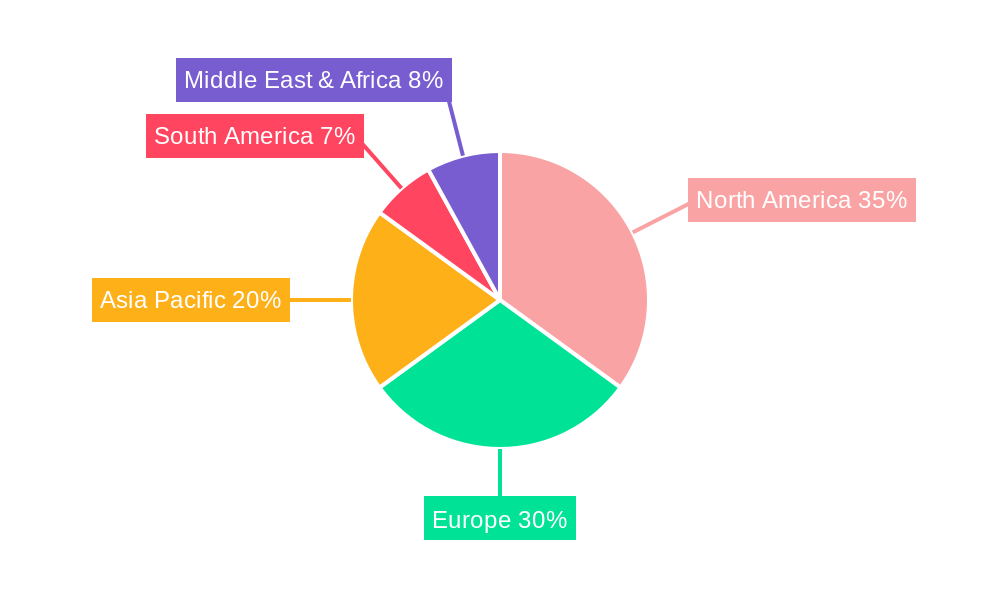

The market's trajectory is further bolstered by supportive healthcare policies and technological innovations leading to improved product performance and patient outcomes. While the rising costs associated with advanced anti-adhesion barrier gels and a limited understanding among some patient populations about their benefits pose minor restraints, the overall market sentiment remains highly optimistic. Key market players are actively engaged in research and development to introduce novel formulations and expand their geographical reach. North America and Europe are expected to remain dominant regions, owing to advanced healthcare infrastructure and higher adoption rates of advanced surgical technologies. However, the Asia Pacific region is anticipated to exhibit the fastest growth, driven by increasing healthcare expenditure, a growing patient pool, and a surge in minimally invasive surgical procedures.

Anti-adhesion Barrier Gel for Medical Market Composition & Trends

The global Anti-adhesion Barrier Gel for Medical market is characterized by a dynamic and evolving landscape, driven by increasing surgical complexity and a growing emphasis on post-operative recovery. Market concentration is moderate, with key players like FzioMed, Endotherapeutics, SEMICAL, KEBOMED, Anika, Ethicon, Shin Poong Pharm, and Hangzhou Singclean Medical Products contributing significantly. Innovation catalysts are primarily focused on enhancing biocompatibility, biodegradability, and ease of application for these critical medical devices. The regulatory landscape varies across regions, with stringent approvals required for new product entrants, influencing market accessibility and competition. Substitute products, though present in some applications, struggle to replicate the targeted and localized efficacy of anti-adhesion barrier gels. End-user profiles are diverse, encompassing surgeons across various specialties, hospital procurement departments, and research institutions. Merger and acquisition (M&A) activities have been a strategic tool for market expansion and technology integration, with recent deal values estimated in the hundreds of millions, further shaping market share distribution. The market is witnessing a steady inflow of investment, particularly into companies demonstrating strong R&D pipelines and established market presence.

- Market Share Distribution: Driven by product innovation and strategic partnerships, leading companies command significant market influence.

- M&A Deal Values: Recent transactions indicate a trend of consolidation, with deal values ranging from XX million to XXX million.

- Innovation Catalysts: Focus on advanced biomaterials and targeted delivery systems to minimize tissue adherence and improve patient outcomes.

- Regulatory Landscapes: Navigating diverse approval pathways across major global markets is a key determinant of market entry and growth.

Anti-adhesion Barrier Gel for Medical Industry Evolution

The Anti-adhesion Barrier Gel for Medical industry has undergone a significant evolution, driven by an escalating demand for advanced surgical solutions that mitigate the adverse effects of post-operative adhesions. Throughout the historical period from 2019 to 2024, the market witnessed consistent growth, fueled by increasing awareness among healthcare professionals and patients regarding the detrimental impact of adhesions on surgical outcomes and quality of life. This period saw substantial investment in research and development, leading to the introduction of novel formulations and improved delivery mechanisms that enhance efficacy and patient comfort. The base year of 2025 marks a crucial point, with the market poised for accelerated expansion. Projections indicate a robust compound annual growth rate (CAGR) of approximately XX% during the forecast period of 2025–2033. This sustained growth trajectory is underpinned by several key factors, including the increasing volume of minimally invasive surgeries, where the application of anti-adhesion barriers is becoming standard practice to prevent complications. Technological advancements have been pivotal, with the development of bioresorbable gels that degrade naturally within the body, eliminating the need for secondary removal procedures and reducing the risk of further tissue irritation. Furthermore, shifts in consumer demands are playing an increasingly important role. Patients are becoming more informed and proactive in seeking treatments that minimize pain and recovery time. This has created a greater impetus for healthcare providers to adopt advanced solutions like anti-adhesion barrier gels. The industry's evolution is also marked by a growing emphasis on the development of gels with enhanced rheological properties for better spreadability and retention at the surgical site, ensuring optimal barrier protection. The study period from 2019 to 2033 encapsulates this dynamic journey, highlighting a market that is not only expanding in size but also maturing in its technological sophistication and clinical application, promising significant advancements in patient care and surgical success rates.

Leading Regions, Countries, or Segments in Anti-adhesion Barrier Gel for Medical

The Anti-adhesion Barrier Gel for Medical market's dominance is a multifaceted phenomenon, intricately linked to regional healthcare infrastructure, surgical procedure volumes, and regulatory frameworks. North America and Europe currently lead the market due to their well-established healthcare systems, high prevalence of complex surgical procedures, and a strong emphasis on patient outcomes and advanced medical technologies. Within these regions, countries like the United States and Germany are significant contributors, driven by substantial investment in medical research and a high adoption rate of innovative surgical aids. Asia Pacific, particularly China and Japan, represents a rapidly growing segment, propelled by an expanding healthcare sector, increasing disposable incomes, and government initiatives to improve healthcare access.

In terms of Application, the Peritoneum segment holds a dominant position. This is largely attributed to the high incidence of abdominal surgeries, such as general surgery, gynecology, and colorectal procedures, where post-operative adhesions are a common and significant complication. The development of specialized gels for peritoneal application has been extensive, offering tailored solutions for this critical surgical field. The Spine segment is emerging as a fast-growing area, driven by the increasing number of spinal fusion and reconstructive surgeries. Adhesion formation in the spinal region can lead to severe neurological complications, making anti-adhesion barrier gels crucial for preventing such adverse events. The Tendon application segment, while smaller, is also experiencing growth, particularly in orthopedic surgeries involving tendon repair, where adhesions can severely impair joint mobility and function.

Considering Types, the Injectable Type currently dominates the market. This form factor offers precise delivery directly to the surgical site, ensuring targeted application and optimal barrier formation. Its ease of use and ability to navigate complex anatomical structures make it a preferred choice for many surgical procedures. The Spread Type is gaining traction due to its ease of application over larger surgical surfaces and its ability to conform to irregular tissue contours. Ongoing research is focused on improving the viscosity and adherence properties of spreadable gels to ensure sustained coverage and effective adhesion prevention.

Dominant Application Segment: Peritoneum

- Key Drivers: High volume of abdominal surgeries (general, gynecological, colorectal), significant complication rates from adhesions, and continuous innovation in peritoneal barrier gels.

- Investment Trends: Substantial R&D investment by leading companies focusing on enhanced biocompatibility and bioresorbability for peritoneal applications.

- Regulatory Support: Favorable regulatory pathways in major markets for products addressing common post-surgical complications in abdominal procedures.

Emerging Application Segment: Spine

- Key Drivers: Rising prevalence of spinal surgeries, critical need to prevent neurological complications from adhesions, and development of specialized gels for spinal site application.

- Technological Advancements: Focus on gels with superior viscosity and hemostatic properties for spinal use.

- Growth Trajectory: Projected high CAGR due to the increasing complexity of spinal interventions.

Dominant Type: Injectable Type

- Key Drivers: Precision in delivery, ease of use in complex anatomies, and wide adoption across various surgical specialties.

- Performance Metrics: High efficacy in forming a localized barrier, leading to reduced adhesion formation.

- Market Penetration: Established market presence with a broad range of products available.

Growing Type: Spread Type

- Key Drivers: Applicability to larger surgical areas, improved patient comfort, and ongoing innovation in material science for better adhesion and spreadability.

- Technological Focus: Development of gels with optimized rheology and prolonged residence time.

- Adoption Rate: Increasing adoption in procedures requiring coverage of extensive surgical fields.

Anti-adhesion Barrier Gel for Medical Product Innovations

Recent product innovations in Anti-adhesion Barrier Gel for Medical are significantly enhancing surgical outcomes and patient recovery. Companies are focusing on developing bioresorbable gels with improved viscoelastic properties, ensuring sustained presence at the surgical site while minimizing foreign body response. Innovations include gels formulated with hyaluronic acid derivatives and polyethylene glycol (PEG) composites, offering superior biocompatibility and predictable degradation profiles. Furthermore, advancements in delivery systems, such as pre-filled syringes with specialized applicators, allow for more precise and efficient application, even in challenging surgical environments. The integration of hemostatic agents within these gels is also a notable innovation, addressing bleeding concerns concurrently with adhesion prevention. These advancements translate to reduced operating times, fewer complications, and faster patient rehabilitation, setting new benchmarks in surgical care.

Propelling Factors for Anti-adhesion Barrier Gel for Medical Growth

The growth of the Anti-adhesion Barrier Gel for Medical market is propelled by a confluence of factors. Increasing awareness of the detrimental impact of post-operative adhesions on patient morbidity and healthcare costs is a primary driver. This awareness encourages surgeons to adopt preventative measures. Advancements in surgical techniques, particularly the rise of minimally invasive surgery (MIS), necessitate effective adhesion prevention strategies to maintain the integrity of surgical planes. Technological innovations, such as the development of advanced biocompatible and bioresorbable polymers, are creating more effective and safer gel formulations. Favorable reimbursement policies and increasing healthcare expenditure globally also contribute significantly, making these advanced medical devices more accessible.

- Increased Surgical Procedure Volumes: Growing number of complex surgeries worldwide.

- Technological Advancements: Development of novel biomaterials and delivery systems.

- Growing Awareness: Enhanced understanding of adhesion-related complications among healthcare professionals and patients.

- Supportive Reimbursement Policies: Government and insurance coverage for anti-adhesion barrier gels.

Obstacles in the Anti-adhesion Barrier Gel for Medical Market

Despite its promising growth, the Anti-adhesion Barrier Gel for Medical market faces several obstacles. High manufacturing costs associated with advanced biomaterials and stringent regulatory approval processes in various countries can deter new entrants and slow down market expansion. The perceived cost-effectiveness of these gels compared to traditional surgical practices can be a barrier for some healthcare systems, particularly in price-sensitive markets. Furthermore, the availability of alternative, albeit less effective, adhesion prevention methods, such as meticulous surgical technique and irrigation, can pose a competitive challenge. Potential side effects, though rare, such as foreign body reactions or localized inflammation, can also lead to hesitancy in adoption.

- High Manufacturing Costs: Expenses associated with developing and producing advanced biomaterials.

- Stringent Regulatory Hurdles: Lengthy and costly approval processes in different geographical regions.

- Cost-Sensitivity: Hesitancy from some healthcare providers to adopt due to perceived high costs.

- Availability of Alternatives: Competition from less sophisticated but cheaper adhesion prevention methods.

Future Opportunities in Anti-adhesion Barrier Gel for Medical

The future of the Anti-adhesion Barrier Gel for Medical market is ripe with opportunities. The expanding scope of applications in new surgical specialties, such as neurosurgery and cardiovascular surgery, presents a significant growth avenue. The development of "smart" gels that can deliver therapeutic agents or actively promote tissue healing alongside adhesion prevention is a promising area for innovation. Emerging markets with rapidly developing healthcare infrastructures offer vast untapped potential. Furthermore, advancements in personalized medicine, leading to tailored anti-adhesion barrier solutions based on individual patient risk factors, could revolutionize the market.

- Expansion into New Surgical Fields: Application in neurosurgery, cardiovascular surgery, and other specialized areas.

- Development of "Smart" Gels: Incorporating therapeutic delivery or active healing properties.

- Growth in Emerging Markets: Untapped potential in developing economies with improving healthcare systems.

- Personalized Medicine: Tailoring gels based on individual patient risk profiles.

Major Players in the Anti-adhesion Barrier Gel for Medical Ecosystem

- FzioMed

- Endotherapeutics

- SEMICAL

- KEBOMED

- Anika

- Ethicon

- Shin Poong Pharm

- Hangzhou Singclean Medical Products

Key Developments in Anti-adhesion Barrier Gel for Medical Industry

- 2024: Launch of a new bioresorbable peritoneal adhesion barrier gel with enhanced spreadability by Hangzhou Singclean Medical Products.

- 2023: FzioMed secures FDA approval for its advanced spinal adhesion barrier gel, expanding its product portfolio.

- 2023: Endotherapeutics announces a strategic partnership with a leading research institute to develop next-generation adhesion prevention technologies.

- 2022: SEMICAL introduces an injectable adhesion barrier gel with improved hemostatic properties for gynecological surgeries.

- 2021: KEBOMED expands its distribution network in the European market for its range of anti-adhesion barrier products.

- 2020: Anika Therapeutics receives CE Mark for its novel spreadable adhesion barrier gel for orthopedic applications.

- 2019: Shin Poong Pharm launches its first injectable anti-adhesion barrier gel in select Asian markets.

- 2019: Ethicon continues to invest in R&D for advanced adhesion prevention solutions, focusing on minimally invasive procedures.

Strategic Anti-adhesion Barrier Gel for Medical Market Forecast

The strategic forecast for the Anti-adhesion Barrier Gel for Medical market indicates robust and sustained growth throughout the study period of 2019–2033. The market is expected to be driven by an increasing global prevalence of surgical procedures, particularly those associated with chronic conditions and aging populations. Innovations in biomaterials and drug delivery systems will continue to enhance product efficacy and patient safety, broadening the application spectrum into more complex surgical interventions. Favorable regulatory environments in key regions and expanding healthcare infrastructure in emerging economies will further catalyze market penetration. Strategic collaborations and M&A activities are anticipated to consolidate market share and drive technological advancements, ensuring that anti-adhesion barrier gels remain a cornerstone of optimal surgical care and improved patient outcomes. The market's potential is further amplified by a growing emphasis on reducing healthcare costs associated with post-operative complications, positioning these gels as an essential preventative tool.

Anti-adhesion Barrier Gel for Medical Segmentation

-

1. Application

- 1.1. Peritoneum

- 1.2. Spine

- 1.3. Tendon

- 1.4. Others

-

2. Types

- 2.1. Injectable Type

- 2.2. Spread Type

- 2.3. Others

Anti-adhesion Barrier Gel for Medical Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Anti-adhesion Barrier Gel for Medical REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Anti-adhesion Barrier Gel for Medical Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Peritoneum

- 5.1.2. Spine

- 5.1.3. Tendon

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Injectable Type

- 5.2.2. Spread Type

- 5.2.3. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Anti-adhesion Barrier Gel for Medical Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Peritoneum

- 6.1.2. Spine

- 6.1.3. Tendon

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Injectable Type

- 6.2.2. Spread Type

- 6.2.3. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Anti-adhesion Barrier Gel for Medical Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Peritoneum

- 7.1.2. Spine

- 7.1.3. Tendon

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Injectable Type

- 7.2.2. Spread Type

- 7.2.3. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Anti-adhesion Barrier Gel for Medical Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Peritoneum

- 8.1.2. Spine

- 8.1.3. Tendon

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Injectable Type

- 8.2.2. Spread Type

- 8.2.3. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Anti-adhesion Barrier Gel for Medical Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Peritoneum

- 9.1.2. Spine

- 9.1.3. Tendon

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Injectable Type

- 9.2.2. Spread Type

- 9.2.3. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Anti-adhesion Barrier Gel for Medical Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Peritoneum

- 10.1.2. Spine

- 10.1.3. Tendon

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Injectable Type

- 10.2.2. Spread Type

- 10.2.3. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 FzioMed

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Endotherapeutics

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 SEMICAL

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 KEBOMED

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Anika

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Ethicon

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Shin Poong Pharm

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Hangzhou Singclean Medical Products

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.1 FzioMed

List of Figures

- Figure 1: Global Anti-adhesion Barrier Gel for Medical Revenue Breakdown (million, %) by Region 2024 & 2032

- Figure 2: North America Anti-adhesion Barrier Gel for Medical Revenue (million), by Application 2024 & 2032

- Figure 3: North America Anti-adhesion Barrier Gel for Medical Revenue Share (%), by Application 2024 & 2032

- Figure 4: North America Anti-adhesion Barrier Gel for Medical Revenue (million), by Types 2024 & 2032

- Figure 5: North America Anti-adhesion Barrier Gel for Medical Revenue Share (%), by Types 2024 & 2032

- Figure 6: North America Anti-adhesion Barrier Gel for Medical Revenue (million), by Country 2024 & 2032

- Figure 7: North America Anti-adhesion Barrier Gel for Medical Revenue Share (%), by Country 2024 & 2032

- Figure 8: South America Anti-adhesion Barrier Gel for Medical Revenue (million), by Application 2024 & 2032

- Figure 9: South America Anti-adhesion Barrier Gel for Medical Revenue Share (%), by Application 2024 & 2032

- Figure 10: South America Anti-adhesion Barrier Gel for Medical Revenue (million), by Types 2024 & 2032

- Figure 11: South America Anti-adhesion Barrier Gel for Medical Revenue Share (%), by Types 2024 & 2032

- Figure 12: South America Anti-adhesion Barrier Gel for Medical Revenue (million), by Country 2024 & 2032

- Figure 13: South America Anti-adhesion Barrier Gel for Medical Revenue Share (%), by Country 2024 & 2032

- Figure 14: Europe Anti-adhesion Barrier Gel for Medical Revenue (million), by Application 2024 & 2032

- Figure 15: Europe Anti-adhesion Barrier Gel for Medical Revenue Share (%), by Application 2024 & 2032

- Figure 16: Europe Anti-adhesion Barrier Gel for Medical Revenue (million), by Types 2024 & 2032

- Figure 17: Europe Anti-adhesion Barrier Gel for Medical Revenue Share (%), by Types 2024 & 2032

- Figure 18: Europe Anti-adhesion Barrier Gel for Medical Revenue (million), by Country 2024 & 2032

- Figure 19: Europe Anti-adhesion Barrier Gel for Medical Revenue Share (%), by Country 2024 & 2032

- Figure 20: Middle East & Africa Anti-adhesion Barrier Gel for Medical Revenue (million), by Application 2024 & 2032

- Figure 21: Middle East & Africa Anti-adhesion Barrier Gel for Medical Revenue Share (%), by Application 2024 & 2032

- Figure 22: Middle East & Africa Anti-adhesion Barrier Gel for Medical Revenue (million), by Types 2024 & 2032

- Figure 23: Middle East & Africa Anti-adhesion Barrier Gel for Medical Revenue Share (%), by Types 2024 & 2032

- Figure 24: Middle East & Africa Anti-adhesion Barrier Gel for Medical Revenue (million), by Country 2024 & 2032

- Figure 25: Middle East & Africa Anti-adhesion Barrier Gel for Medical Revenue Share (%), by Country 2024 & 2032

- Figure 26: Asia Pacific Anti-adhesion Barrier Gel for Medical Revenue (million), by Application 2024 & 2032

- Figure 27: Asia Pacific Anti-adhesion Barrier Gel for Medical Revenue Share (%), by Application 2024 & 2032

- Figure 28: Asia Pacific Anti-adhesion Barrier Gel for Medical Revenue (million), by Types 2024 & 2032

- Figure 29: Asia Pacific Anti-adhesion Barrier Gel for Medical Revenue Share (%), by Types 2024 & 2032

- Figure 30: Asia Pacific Anti-adhesion Barrier Gel for Medical Revenue (million), by Country 2024 & 2032

- Figure 31: Asia Pacific Anti-adhesion Barrier Gel for Medical Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Anti-adhesion Barrier Gel for Medical Revenue million Forecast, by Region 2019 & 2032

- Table 2: Global Anti-adhesion Barrier Gel for Medical Revenue million Forecast, by Application 2019 & 2032

- Table 3: Global Anti-adhesion Barrier Gel for Medical Revenue million Forecast, by Types 2019 & 2032

- Table 4: Global Anti-adhesion Barrier Gel for Medical Revenue million Forecast, by Region 2019 & 2032

- Table 5: Global Anti-adhesion Barrier Gel for Medical Revenue million Forecast, by Application 2019 & 2032

- Table 6: Global Anti-adhesion Barrier Gel for Medical Revenue million Forecast, by Types 2019 & 2032

- Table 7: Global Anti-adhesion Barrier Gel for Medical Revenue million Forecast, by Country 2019 & 2032

- Table 8: United States Anti-adhesion Barrier Gel for Medical Revenue (million) Forecast, by Application 2019 & 2032

- Table 9: Canada Anti-adhesion Barrier Gel for Medical Revenue (million) Forecast, by Application 2019 & 2032

- Table 10: Mexico Anti-adhesion Barrier Gel for Medical Revenue (million) Forecast, by Application 2019 & 2032

- Table 11: Global Anti-adhesion Barrier Gel for Medical Revenue million Forecast, by Application 2019 & 2032

- Table 12: Global Anti-adhesion Barrier Gel for Medical Revenue million Forecast, by Types 2019 & 2032

- Table 13: Global Anti-adhesion Barrier Gel for Medical Revenue million Forecast, by Country 2019 & 2032

- Table 14: Brazil Anti-adhesion Barrier Gel for Medical Revenue (million) Forecast, by Application 2019 & 2032

- Table 15: Argentina Anti-adhesion Barrier Gel for Medical Revenue (million) Forecast, by Application 2019 & 2032

- Table 16: Rest of South America Anti-adhesion Barrier Gel for Medical Revenue (million) Forecast, by Application 2019 & 2032

- Table 17: Global Anti-adhesion Barrier Gel for Medical Revenue million Forecast, by Application 2019 & 2032

- Table 18: Global Anti-adhesion Barrier Gel for Medical Revenue million Forecast, by Types 2019 & 2032

- Table 19: Global Anti-adhesion Barrier Gel for Medical Revenue million Forecast, by Country 2019 & 2032

- Table 20: United Kingdom Anti-adhesion Barrier Gel for Medical Revenue (million) Forecast, by Application 2019 & 2032

- Table 21: Germany Anti-adhesion Barrier Gel for Medical Revenue (million) Forecast, by Application 2019 & 2032

- Table 22: France Anti-adhesion Barrier Gel for Medical Revenue (million) Forecast, by Application 2019 & 2032

- Table 23: Italy Anti-adhesion Barrier Gel for Medical Revenue (million) Forecast, by Application 2019 & 2032

- Table 24: Spain Anti-adhesion Barrier Gel for Medical Revenue (million) Forecast, by Application 2019 & 2032

- Table 25: Russia Anti-adhesion Barrier Gel for Medical Revenue (million) Forecast, by Application 2019 & 2032

- Table 26: Benelux Anti-adhesion Barrier Gel for Medical Revenue (million) Forecast, by Application 2019 & 2032

- Table 27: Nordics Anti-adhesion Barrier Gel for Medical Revenue (million) Forecast, by Application 2019 & 2032

- Table 28: Rest of Europe Anti-adhesion Barrier Gel for Medical Revenue (million) Forecast, by Application 2019 & 2032

- Table 29: Global Anti-adhesion Barrier Gel for Medical Revenue million Forecast, by Application 2019 & 2032

- Table 30: Global Anti-adhesion Barrier Gel for Medical Revenue million Forecast, by Types 2019 & 2032

- Table 31: Global Anti-adhesion Barrier Gel for Medical Revenue million Forecast, by Country 2019 & 2032

- Table 32: Turkey Anti-adhesion Barrier Gel for Medical Revenue (million) Forecast, by Application 2019 & 2032

- Table 33: Israel Anti-adhesion Barrier Gel for Medical Revenue (million) Forecast, by Application 2019 & 2032

- Table 34: GCC Anti-adhesion Barrier Gel for Medical Revenue (million) Forecast, by Application 2019 & 2032

- Table 35: North Africa Anti-adhesion Barrier Gel for Medical Revenue (million) Forecast, by Application 2019 & 2032

- Table 36: South Africa Anti-adhesion Barrier Gel for Medical Revenue (million) Forecast, by Application 2019 & 2032

- Table 37: Rest of Middle East & Africa Anti-adhesion Barrier Gel for Medical Revenue (million) Forecast, by Application 2019 & 2032

- Table 38: Global Anti-adhesion Barrier Gel for Medical Revenue million Forecast, by Application 2019 & 2032

- Table 39: Global Anti-adhesion Barrier Gel for Medical Revenue million Forecast, by Types 2019 & 2032

- Table 40: Global Anti-adhesion Barrier Gel for Medical Revenue million Forecast, by Country 2019 & 2032

- Table 41: China Anti-adhesion Barrier Gel for Medical Revenue (million) Forecast, by Application 2019 & 2032

- Table 42: India Anti-adhesion Barrier Gel for Medical Revenue (million) Forecast, by Application 2019 & 2032

- Table 43: Japan Anti-adhesion Barrier Gel for Medical Revenue (million) Forecast, by Application 2019 & 2032

- Table 44: South Korea Anti-adhesion Barrier Gel for Medical Revenue (million) Forecast, by Application 2019 & 2032

- Table 45: ASEAN Anti-adhesion Barrier Gel for Medical Revenue (million) Forecast, by Application 2019 & 2032

- Table 46: Oceania Anti-adhesion Barrier Gel for Medical Revenue (million) Forecast, by Application 2019 & 2032

- Table 47: Rest of Asia Pacific Anti-adhesion Barrier Gel for Medical Revenue (million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Anti-adhesion Barrier Gel for Medical?

The projected CAGR is approximately XX%.

2. Which companies are prominent players in the Anti-adhesion Barrier Gel for Medical?

Key companies in the market include FzioMed, Endotherapeutics, SEMICAL, KEBOMED, Anika, Ethicon, Shin Poong Pharm, Hangzhou Singclean Medical Products.

3. What are the main segments of the Anti-adhesion Barrier Gel for Medical?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Anti-adhesion Barrier Gel for Medical," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Anti-adhesion Barrier Gel for Medical report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Anti-adhesion Barrier Gel for Medical?

To stay informed about further developments, trends, and reports in the Anti-adhesion Barrier Gel for Medical, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence